Total output of goods and services available in an economy, influenced by technology and resource changes, central to explaining economic fluctuations.

Aggregate Demand

Overall spending on goods and services in an economy, affected by production and employment levels, but less emphasized in this model.

Supply Shock

Sudden event causing a change in resource availability or input prices, leading to shifts in production and employment.

Long Run Aggregate Supply

Curve representing the economy’s maximum sustainable output, shifting due to technology or resource changes.

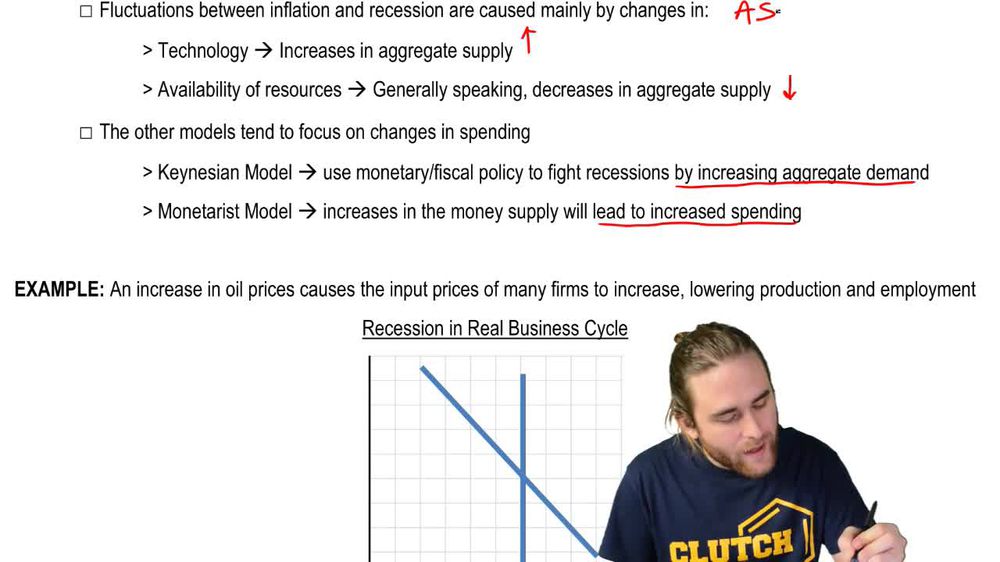

Equilibrium

Point where aggregate supply and aggregate demand intersect, determining real GDP and price level in the economy.

Real GDP

Measure of economic output adjusted for price changes, reflecting actual production levels after supply shocks.

Price Level

Average of current prices across the entire economy, remaining constant during supply-driven recessions in this model.

Recession

Period of reduced economic activity, often triggered by decreased aggregate supply from resource or technology changes.

Inflation

General increase in prices, attributed in this model to supply-side factors rather than demand-side changes.

Resource Availability

Access to inputs needed for production, with reductions causing shifts in aggregate supply and economic downturns.

Input Prices

Costs of resources used by firms, with increases leading to lower production and employment.

Technology

Advancements or changes affecting production efficiency, driving shifts in aggregate supply and economic output.

Employment

Number of people working in the economy, declining when aggregate supply falls due to supply shocks.

Monetarist Model

Economic framework emphasizing money supply’s role in influencing spending and aggregate demand, contrasting with supply focus.

Keynesian Model

Economic theory prioritizing aggregate demand as the main driver of recessions and recovery, differing from supply-side explanations.

Back

Back

03:54

03:54