Skip to main content

Microeconomics

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

Back

Classical Model and Keynesian Model definitions

You can tap to flip the card.

Classical Model

You can tap to flip the card.

👆

Classical Model

Economic framework assuming flexible prices and wages, full employment, and self-correcting markets without government intervention.

Track progress

Control buttons has been changed to "navigation" mode.

1/15

Related flashcards

Recommended videos

Classical Model and Keynesian Model quiz

Classical Model and Keynesian Model

15 Terms

Guided course

03:04

Keynesian Model

Guided course

02:54

Classical Model

Guided course

03:41

Graphical Comparison of Classical Model and Keynesian Model

Terms in this set (15)

Hide definitions

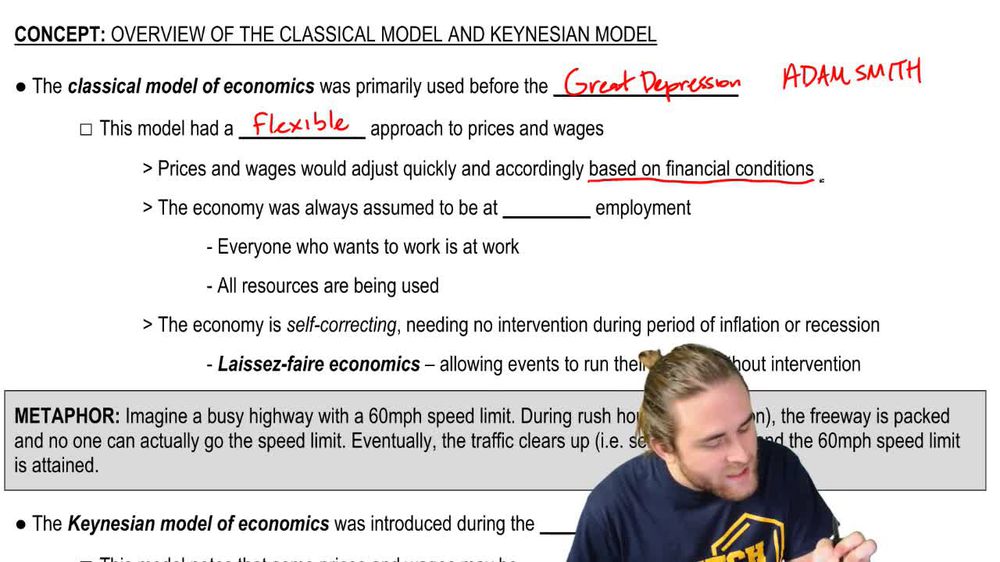

Classical Model

Economic framework assuming flexible prices and wages, full employment, and self-correcting markets without government intervention.

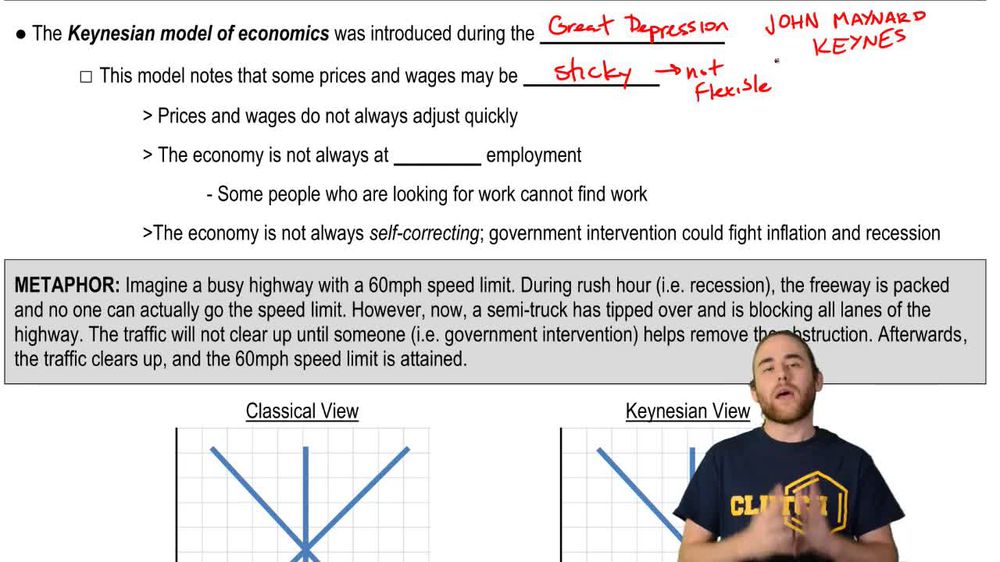

Keynesian Model

Economic theory emphasizing sticky prices and wages, unemployment, and the necessity of government intervention during recessions and inflation.

Flexible Prices

Market condition where prices adjust quickly in response to changes in supply and demand, enabling rapid equilibrium restoration.

Sticky Wages

Situation where wage levels remain unchanged despite shifts in economic conditions, often due to contracts or institutional factors.

Full Employment

State where all available labor resources are being used efficiently, and anyone seeking work can find a job.

Self-Correcting Market

Economic system that naturally returns to equilibrium without external intervention, relying on internal adjustments.

Laissez-Faire

Principle advocating minimal government involvement in economic affairs, allowing markets to operate freely.

Government Intervention

Actions by authorities to influence economic outcomes, such as addressing recessions or inflation through policy measures.

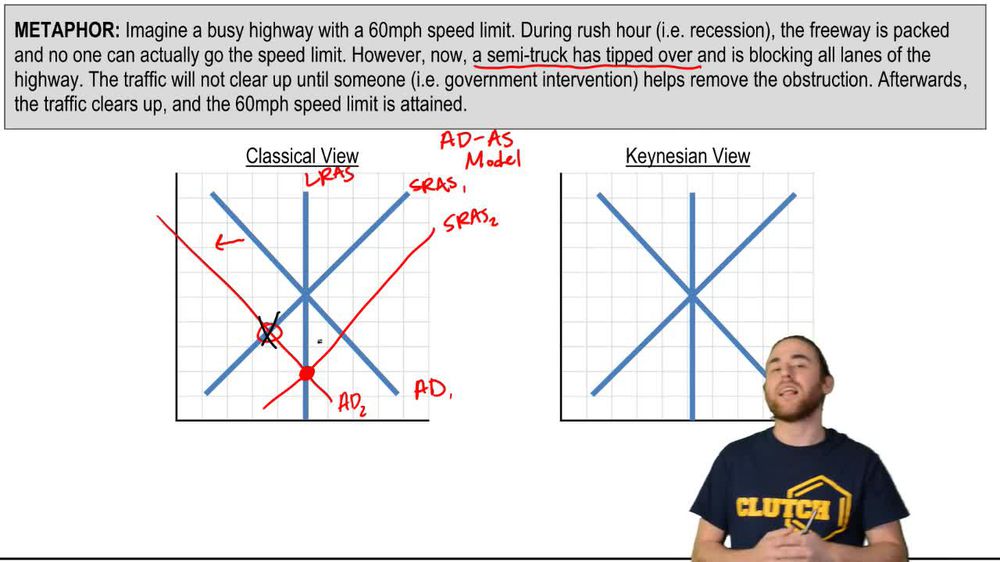

Aggregate Demand

Total spending on goods and services within an economy, represented as a downward-sloping curve in macroeconomic models.

Aggregate Supply

Total output of goods and services produced by an economy, depicted as both short-run and long-run curves in models.

Short Run Equilibrium

Temporary state where aggregate demand and aggregate supply intersect, not necessarily at potential GDP.

Long Run Equilibrium

Condition where aggregate demand, short-run aggregate supply, and long-run aggregate supply meet at potential GDP.

Potential GDP

Maximum sustainable output an economy can produce when all resources are fully employed.

Recession

Period of economic decline marked by reduced aggregate demand, increased unemployment, and lower output.

Invisible Hand

Metaphor for the self-regulating nature of markets, guiding resources to their most efficient uses without direct intervention.

BackBack

BackBack

03:04

03:04