Skip to main content

Macroeconomics

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

Back

Long Run Equilibrium quiz

You can tap to flip the card.

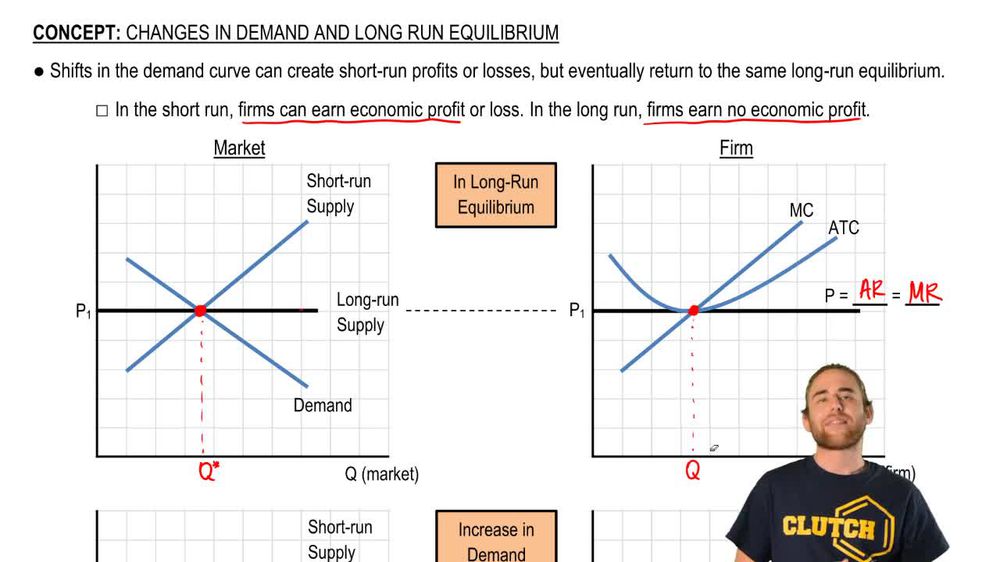

In perfect competition, what condition must be met for long-run equilibrium to occur?

You can tap to flip the card.

👆

In perfect competition, what condition must be met for long-run equilibrium to occur?

Price must equal the minimum average total cost (ATC), resulting in zero economic profit for firms.

Track progress

Control buttons has been changed to "navigation" mode.

1/15

Related flashcards

Recommended videos

Long Run Equilibrium definitions

Long Run Equilibrium

15 Terms

Guided course

07:04

Long Run Equilibrium

Terms in this set (15)

Hide definitions

In perfect competition, what condition must be met for long-run equilibrium to occur?

Price must equal the minimum average total cost (ATC), resulting in zero economic profit for firms.

What happens to market price and quantity when there is an increase in aggregate demand in the short run?

Market price and quantity both increase in the short run, leading to short-run profits for firms.

Why do new firms enter the market when existing firms are earning short-run profits?

New firms are attracted by the opportunity to earn profits, so they enter the market, increasing supply.

What is the effect of new firms entering the market on the market supply curve?

The market supply curve shifts to the right as more firms enter the market.

How does the entry of new firms affect the market price in the long run?

The increased supply causes the market price to fall back to the minimum ATC.

What is the profit situation for firms in long-run equilibrium in perfect competition?

Firms earn zero economic profit because price equals minimum ATC.

What role do marginal cost and marginal revenue play in determining a firm's output?

A firm produces the quantity where marginal cost equals marginal revenue.

What happens to the average total cost and marginal cost curves when demand increases?

The average total cost and marginal cost curves do not change; only the price and quantity change.

After an increase in demand, why do profits eventually disappear in the long run?

Profits disappear because entry of new firms increases supply, lowering price back to minimum ATC.

What happens to the number of firms in the market after a permanent increase in demand?

The number of firms increases to meet the higher demand, but each firm returns to zero economic profit.

In the long run, where does the market price settle after a demand shock?

The market price settles at the minimum average total cost, restoring long-run equilibrium.

What is the relationship between price, average revenue, and marginal revenue in perfect competition?

In perfect competition, price equals both average revenue and marginal revenue.

How do supply shocks or demand fluctuations affect long-run equilibrium?

They cause short-run profits or losses, but entry or exit of firms restores long-run equilibrium at minimum ATC.

What happens to the quantity supplied in the market after an increase in demand and entry of new firms?

The total quantity supplied increases to satisfy the higher demand.

Why is understanding the ATC, MC, and MR curves important for analyzing firm behavior?

These curves help determine the profit-maximizing output and explain how firms adjust to market changes.

BackBack

BackBack

07:04

07:04