Skip to main content

Macroeconomics

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

Back

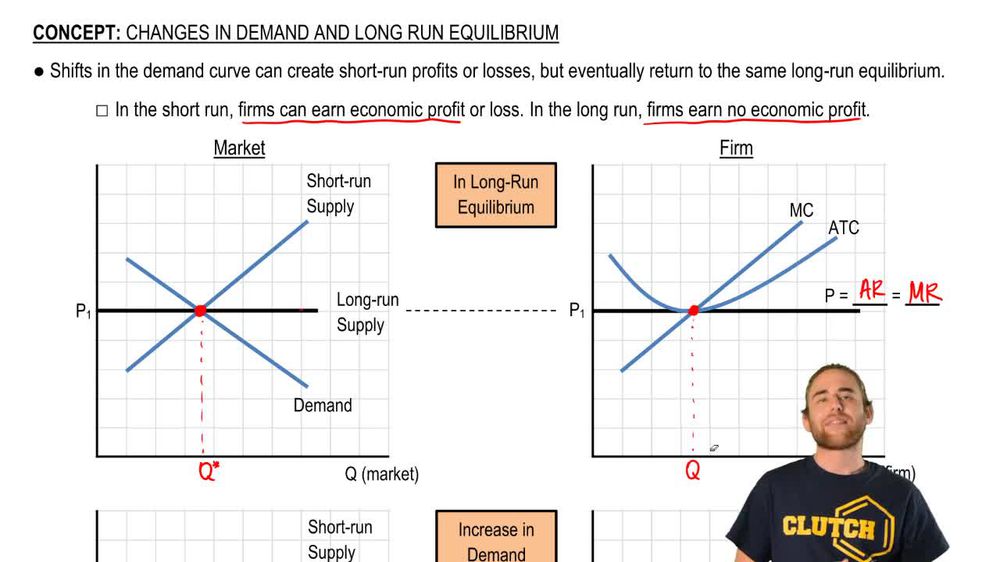

Long Run Equilibrium definitions

You can tap to flip the card.

Long Run Equilibrium

You can tap to flip the card.

👆

Long Run Equilibrium

A market state where price equals minimum average total cost and firms earn zero economic profit, even after demand or supply changes.

Track progress

Control buttons has been changed to "navigation" mode.

1/15

Related flashcards

Recommended videos

Long Run Equilibrium quiz

Long Run Equilibrium

15 Terms

Guided course

07:04

Long Run Equilibrium

Terms in this set (15)

Hide definitions

Long Run Equilibrium

A market state where price equals minimum average total cost and firms earn zero economic profit, even after demand or supply changes.

Perfect Competition

A market structure with many firms selling identical products, allowing free entry and exit, and no single firm can influence price.

Average Total Cost

A firm's total cost divided by output, showing the per-unit cost of production at various output levels.

Marginal Cost

The additional cost incurred from producing one more unit of output, crucial for determining optimal production.

Marginal Revenue

The extra revenue gained from selling one more unit, equal to price in perfectly competitive markets.

Economic Profit

The difference between total revenue and total costs, including opportunity costs; zero in long-run equilibrium.

Demand Curve

A graphical representation showing the relationship between price and quantity demanded at various prices.

Supply Curve

A graphical representation showing the relationship between price and quantity supplied at various prices.

Entry

The process by which new firms join a market, typically attracted by short-run profits, increasing market supply.

Exit

The process by which firms leave a market, usually due to losses, reducing market supply.

Aggregate Demand

The total demand for a product in the market, influencing price and quantity when it shifts.

Market Supply

The total quantity of a good that all firms in a market are willing to sell at each price.

Zero Economic Profit

A situation where total revenue equals total costs, including opportunity costs, leaving no incentive for entry or exit.

Short Run Profit

A temporary situation where firms earn above-normal returns due to a sudden increase in demand.

Minimum ATC

The lowest point on the average total cost curve, indicating the most efficient scale of production.

BackBack

BackBack

07:04

07:04