Skip to main content

Macroeconomics

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

Back

Four Market Model Summary: Perfect Competition quiz

You can tap to flip the card.

What is the typical number of firms in a perfectly competitive market?

You can tap to flip the card.

👆

What is the typical number of firms in a perfectly competitive market?

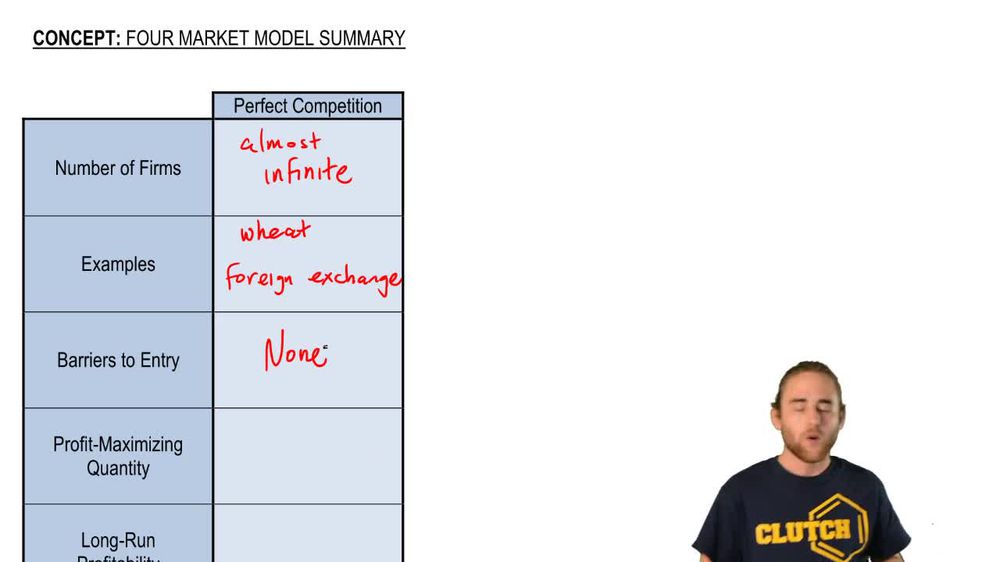

There are an almost infinite number of firms, so no single firm can influence the market price.

Track progress

Control buttons has been changed to "navigation" mode.

1/15

Related flashcards

Recommended videos

Four Market Model Summary: Perfect Competition definitions

Four Market Model Summary: Perfect Competition

14 Terms

Guided course

05:02

Four Market Model Summary: Perfect Competition

Terms in this set (15)

Hide definitions

What is the typical number of firms in a perfectly competitive market?

There are an almost infinite number of firms, so no single firm can influence the market price.

Give two common examples of perfectly competitive markets.

Wheat markets and foreign exchange markets are common examples of perfect competition.

What does it mean for firms to be 'price takers' in perfect competition?

It means firms must accept the market price and cannot influence it by their own actions.

Are there barriers to entry in perfect competition?

No, there are no barriers to entry; firms can freely enter and exit the market.

At what point do firms in perfect competition maximize profit?

Firms maximize profit where marginal revenue equals marginal cost (MR=MC).

What is the relationship between price, average revenue, and marginal revenue in perfect competition?

In perfect competition, price equals both average revenue and marginal revenue.

What happens to economic profit in the long run in perfect competition?

In the long run, firms earn zero economic profit because price equals average total cost.

Why does price equal marginal cost in perfect competition?

Because firms produce where marginal revenue equals marginal cost, and price equals marginal revenue, so price equals marginal cost.

What type of efficiency is achieved in perfect competition?

Both allocative and productive efficiency are achieved in perfect competition.

What does zero economic profit mean for firms in perfect competition?

It means firms cover all their costs, including opportunity costs, but do not earn extra profit.

How does free entry and exit affect long-run profits in perfect competition?

Free entry and exit ensure that any economic profit is competed away, leading to zero economic profit in the long run.

What is a barrier to entry?

A barrier to entry is something that prevents new firms from entering a market.

How does perfect competition illustrate the principles of supply and demand?

It shows how prices are determined by the interaction of many buyers and sellers, with no single firm able to set the price.

What is the profit-maximizing rule for firms in perfect competition?

Firms maximize profit by producing the quantity where marginal revenue equals marginal cost (MR=MC).

In perfect competition, what does the equality of price and marginal cost imply about resource allocation?

It implies that resources are allocated efficiently, as goods are produced up to the point where the value to consumers equals the cost of production.

BackBack

BackBack

05:02

05:02