Skip to main content

Macroeconomics

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

Back

Four Market Model Summary: Perfect Competition definitions

You can tap to flip the card.

Perfect Competition

You can tap to flip the card.

👆

Perfect Competition

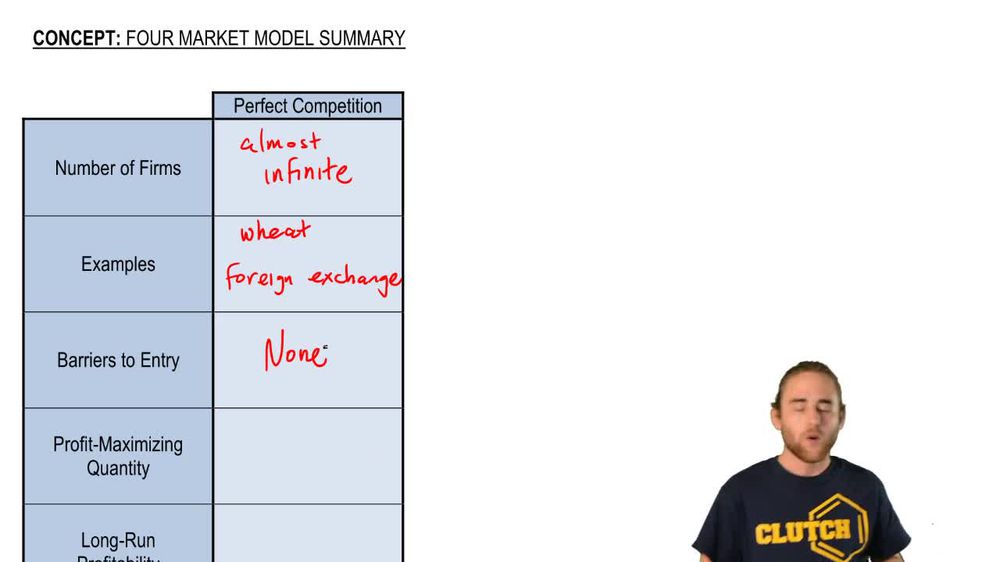

A market structure with countless firms, identical products, and no single firm able to influence price.

Track progress

Control buttons has been changed to "navigation" mode.

1/14

Related flashcards

Recommended videos

Four Market Model Summary: Perfect Competition quiz

Four Market Model Summary: Perfect Competition

15 Terms

Guided course

05:02

Four Market Model Summary: Perfect Competition

Terms in this set (14)

Hide definitions

Perfect Competition

A market structure with countless firms, identical products, and no single firm able to influence price.

Price Taker

A firm that must accept the market price, unable to set its own due to intense competition.

Barriers to Entry

Obstacles preventing new firms from joining a market, absent in this structure.

Marginal Revenue

The additional income from selling one more unit, equal to price in this market.

Marginal Cost

The extra expense of producing one more unit, used to determine optimal output.

Profit Maximizing Quantity

The output level where additional revenue from selling equals the extra cost of producing.

Long-Run Equilibrium

A state where firms earn zero economic profit and price matches average total cost.

Economic Profit

Total revenue minus all costs, including opportunity costs; zero in the long run here.

Average Total Cost

Total cost divided by output, equal to price in long-run equilibrium.

Allocative Efficiency

A condition where resources are distributed so that price equals marginal cost.

Productive Efficiency

A situation where goods are produced at the lowest possible cost, at minimum average total cost.

Average Revenue

Revenue per unit sold, identical to price in this market structure.

Supply

The total amount of a good firms are willing to sell at various prices in the market.

Demand

The total amount of a good consumers are willing to buy at various prices in the market.

BackBack

BackBack

05:02

05:02