Skip to main content

Macroeconomics

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

Back

Four Market Model Summary: Monopolistic Competition quiz

You can tap to flip the card.

How many firms are typically found in monopolistic competition?

You can tap to flip the card.

👆

How many firms are typically found in monopolistic competition?

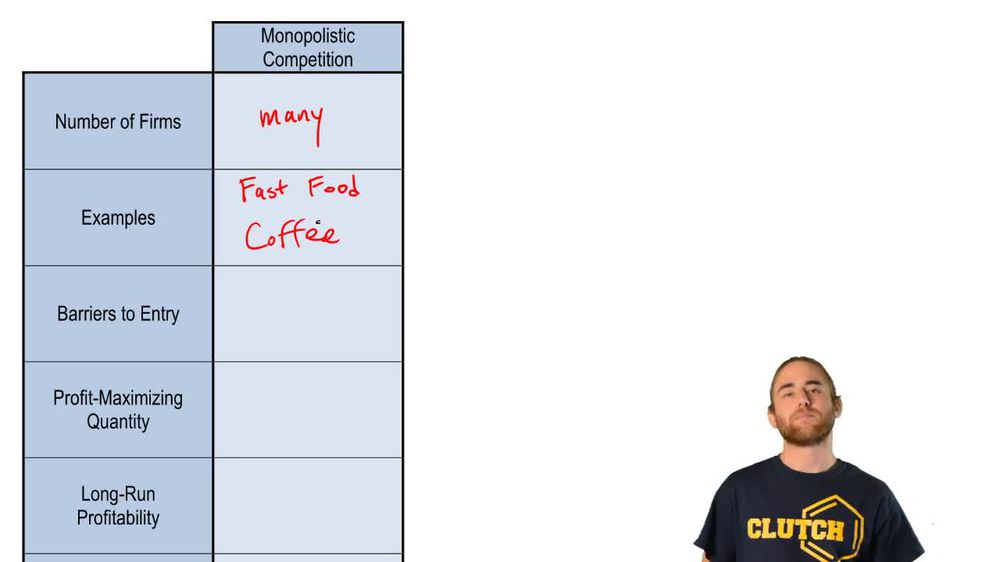

There are many firms in monopolistic competition, though not as many as in perfect competition.

Track progress

Control buttons has been changed to "navigation" mode.

1/15

Related flashcards

Recommended videos

Four Market Model Summary: Monopolistic Competition definitions

Four Market Model Summary: Monopolistic Competition

15 Terms

Guided course

03:30

Four Market Model Summary: Monopolistic Competition

1

views

Terms in this set (15)

Hide definitions

How many firms are typically found in monopolistic competition?

There are many firms in monopolistic competition, though not as many as in perfect competition.

What are two common examples of monopolistically competitive markets?

Fast food and coffee markets are common examples of monopolistically competitive markets.

What is meant by 'barriers to entry' in a market?

Barriers to entry are obstacles that prevent new firms from entering a market.

How do barriers to entry in monopolistic competition compare to perfect competition?

Both have low or no barriers to entry, making it easy for new firms to enter the market.

At what point do firms in monopolistic competition maximize profit?

Firms maximize profit where marginal revenue equals marginal cost (MR = MC).

In the long run, what happens to economic profit in monopolistic competition?

Economic profit becomes zero in the long run because price equals average total cost (P = ATC).

How is price determined for a firm in monopolistic competition?

Price is determined from the demand curve at the profit-maximizing quantity.

What is the relationship between price and marginal revenue in monopolistic competition?

Price is greater than marginal revenue due to the downward-sloping demand curve.

What is the relationship between price and marginal cost in monopolistic competition?

Price is greater than marginal cost, creating a markup over marginal cost.

Why does monopolistic competition have a downward-sloping demand curve?

Because firms have some control over price and can differentiate their products.

What is the equilibrium condition for monopolistic competition in the long run?

The equilibrium condition is where price equals average total cost (P = ATC).

How does monopolistic competition differ from perfect competition in terms of price-setting?

Firms in monopolistic competition are price-setters, while those in perfect competition are price-takers.

What does the markup in monopolistic competition represent?

The markup represents the difference between price and marginal cost.

How can you calculate profit for a firm in monopolistic competition using a graph?

Profit is calculated by finding the difference between price and average total cost at the profit-maximizing quantity.

Why is understanding monopolistic competition important for analyzing market structures?

It highlights differences in price-setting, market entry, and equilibrium conditions compared to other market structures.

BackBack

BackBack

03:30

03:30