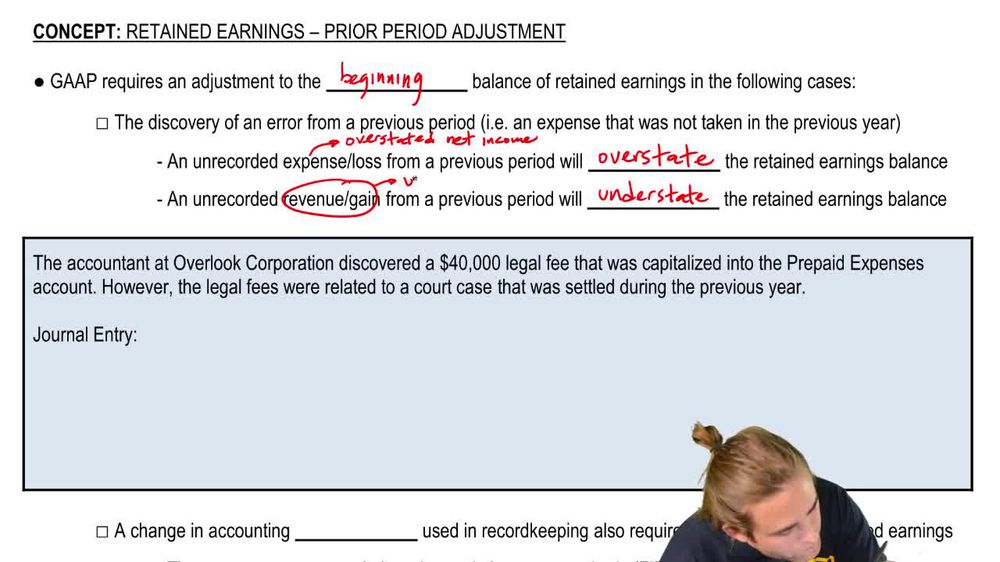

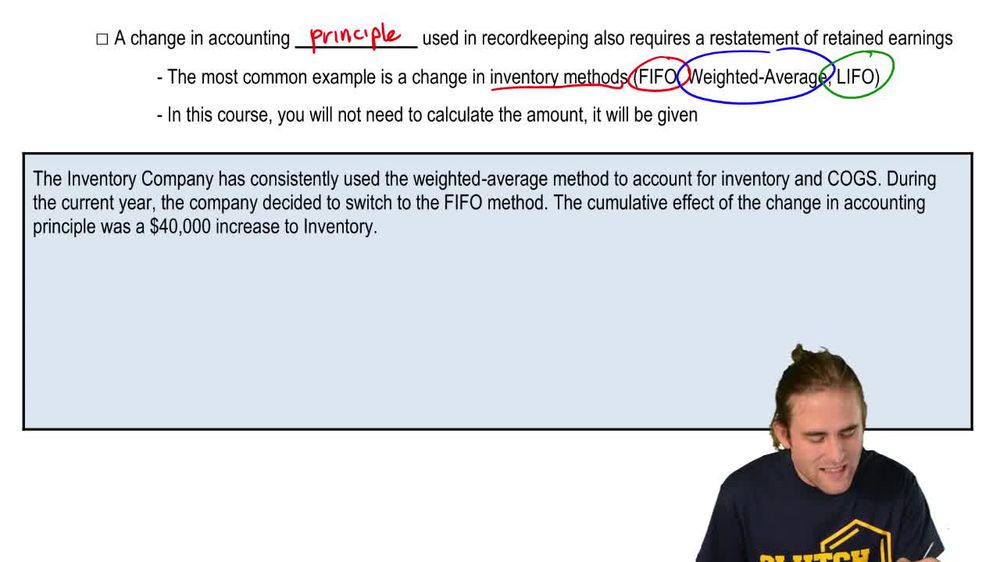

What are prior period adjustments in retained earnings, and when are they necessary?

Prior period adjustments in retained earnings are corrections made to the beginning balance of retained earnings due to errors or changes in accounting principles from previous periods. They are necessary when errors such as unrecorded expenses or revenues are discovered, or when a company changes its accounting principles, like switching inventory methods.

Back

Back

04:17

04:17