What are the main differences between GAAP and IFRS in the presentation of a classified balance sheet?

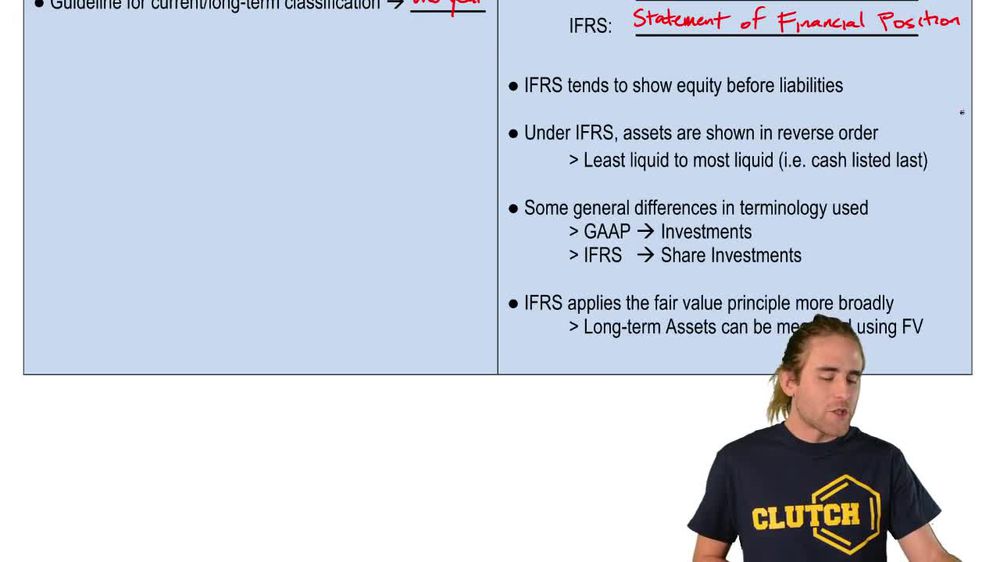

GAAP (used in the USA) and IFRS (used internationally) both require a classified balance sheet dividing assets and liabilities into current and long-term based on a one-year threshold. However, IFRS refers to the balance sheet as the 'Statement of Financial Position,' typically lists equity before liabilities, and presents assets in reverse order of liquidity (long-term assets first, cash last). Additionally, GAAP uses the historical cost principle for asset valuation, while IFRS allows assets to be revalued to fair market value, leading to more current but potentially fluctuating asset values.

Back

Back

06:27

06:27