Skip to main content

Financial Accounting

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

Back

GAAP vs. IFRS: Classified Balance Sheet definitions

You can tap to flip the card.

GAAP

You can tap to flip the card.

👆

GAAP

U.S. accounting standards set by FASB, emphasizing historical cost and a specific balance sheet format.

Track progress

Control buttons has been changed to "navigation" mode.

1/15

Related flashcards

Related practice

Recommended videos

GAAP vs. IFRS: Classified Balance Sheet quiz #1

GAAP vs. IFRS: Classified Balance Sheet

10 Terms

GAAP vs. IFRS: Classified Balance Sheet

15. GAAP vs IFRS

10 problems

Topic

GAAP vs. IFRS: Recording Differences

15. GAAP vs IFRS

10 problems

Topic

15. GAAP vs IFRS

13 topics

13 problems

Chapter

Guided course

06:27

GAAP vs. IFRS: Classified Balance Sheet

2

views

Terms in this set (15)

Hide definitions

GAAP

U.S. accounting standards set by FASB, emphasizing historical cost and a specific balance sheet format.

IFRS

International accounting standards set by IASB, allowing asset revaluation and using different balance sheet terminology.

FASB

U.S. organization responsible for establishing and updating generally accepted accounting principles.

IASB

International body that develops and issues global accounting standards for financial reporting.

Classified Balance Sheet

Financial statement dividing assets and liabilities into current and long-term categories using a one-year threshold.

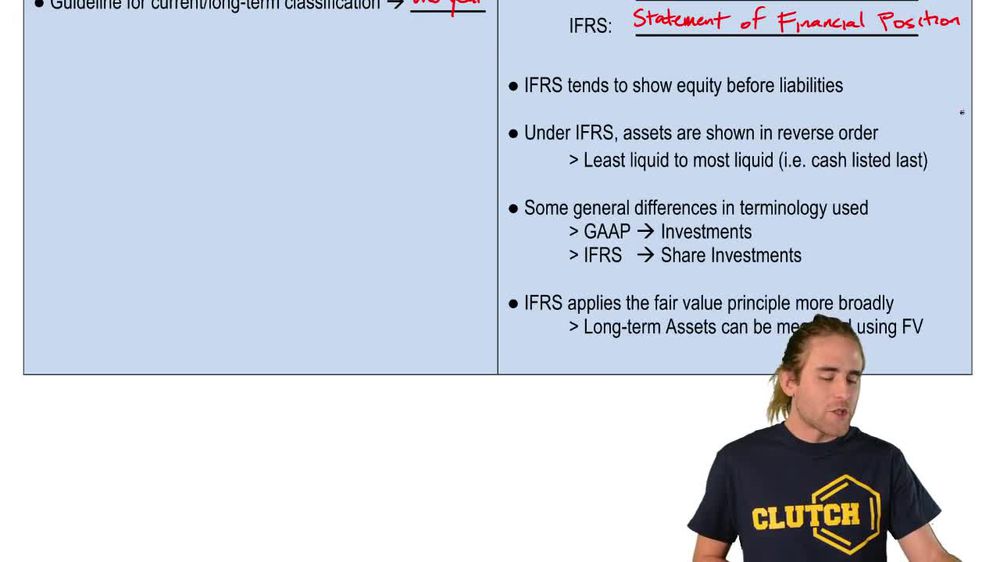

Statement of Financial Position

IFRS term for the balance sheet, typically listing equity before liabilities and assets in reverse liquidity order.

Historical Cost Principle

Accounting guideline requiring assets to be recorded at their original purchase price, ensuring consistency over time.

Fair Value Principle

IFRS guideline allowing assets to be updated to reflect current market values, resulting in more frequent valuation changes.

Current Assets

Resources expected to be converted to cash or used up within one year, such as cash and receivables.

Long-term Assets

Resources expected to provide economic benefit beyond one year, including equipment and long-term investments.

Current Liabilities

Obligations due within one year, such as accounts payable and short-term loans.

Long-term Liabilities

Obligations not due within the next year, including bonds payable and long-term loans.

Equity

Residual interest in assets after deducting liabilities, often presented before liabilities under IFRS.

Liquidity

Measure of how quickly assets can be converted to cash, with IFRS listing assets in reverse order of this characteristic.

Share Investments

IFRS term for investments in other companies' shares, equivalent to 'investments' under GAAP.

BackBack

BackBack

06:27

06:27