Skip to main content

Microeconomics

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

Back

The Production Function and Diminishing Returns definitions

You can tap to flip the card.

Production Function

You can tap to flip the card.

👆

Production Function

Shows how output changes as more inputs are added, mapping workers to pizzas produced in a business.

Track progress

Control buttons has been changed to "navigation" mode.

1/15

Related flashcards

Related practice

Recommended videos

The Production Function and Diminishing Returns quiz #1

The Production Function and Diminishing Returns

13 Terms

The Production Function and Diminishing Returns

10. The Costs of Production

10 problems

Topic

Marginal Cost

10. The Costs of Production

10 problems

Topic

10. The Costs of Production

9 topics

15 problems

Chapter

Guided course

07:45

The Production Function and Diminishing Returns

6

views

Guided course

05:09

Calculating Fixed Cost, Variable Cost, and Average Total Cost

5

views

Terms in this set (15)

Hide definitions

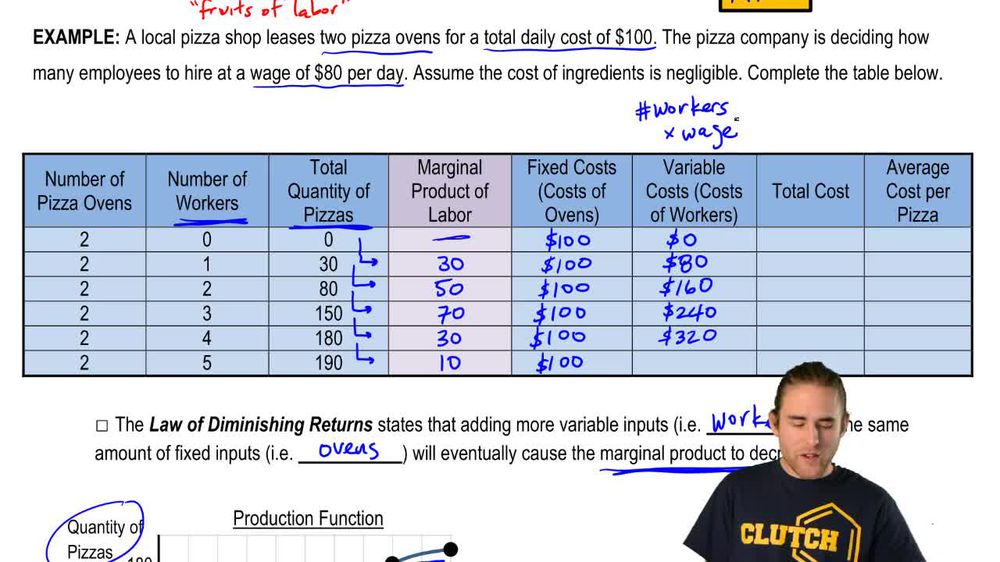

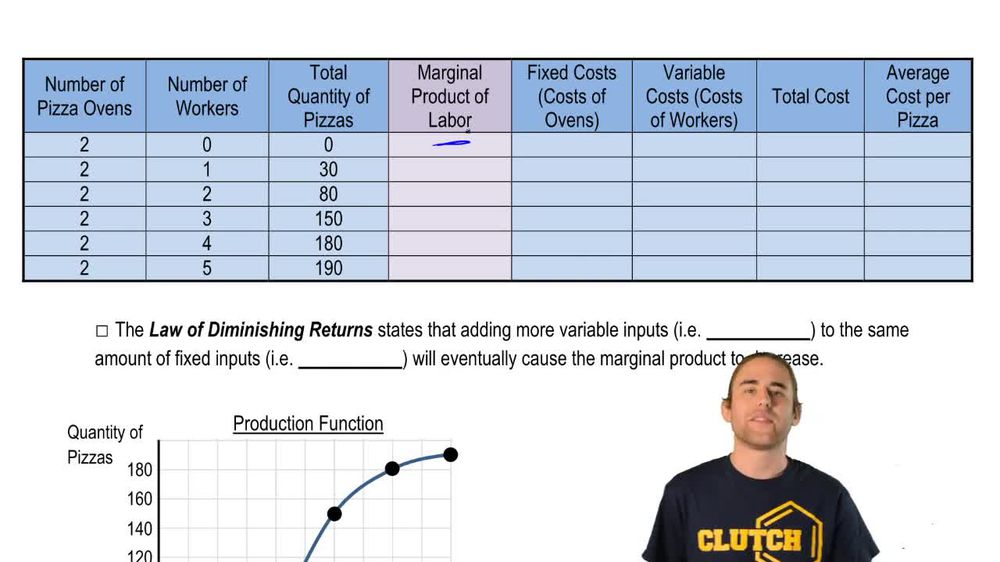

Production Function

Shows how output changes as more inputs are added, mapping workers to pizzas produced in a business.

Marginal Product of Labor

Measures the increase in output from hiring one additional worker, revealing productivity changes.

Fixed Cost

Expense that remains unchanged regardless of output, such as daily oven rental in a pizza shop.

Variable Cost

Expense that rises with increased production, like wages paid for each additional worker hired.

Total Cost

Sum of fixed and variable expenses, representing the overall spending to produce a given output.

Average Cost

Calculated by dividing total expenses by the number of units produced, indicating cost per item.

Law of Diminishing Returns

Describes how adding more workers to fixed resources eventually leads to reduced productivity per worker.

Specialization

Division of tasks among workers, increasing efficiency and output when labor is optimally allocated.

Optimal Point

Moment when adding workers maximizes productivity before diminishing returns begin to reduce gains.

Average Total Cost

Represents the per-unit expense when both fixed and variable costs are considered for all output.

Input

Resource used in production, such as labor or equipment, necessary for creating goods or services.

Output

Quantity of goods produced, like pizzas, resulting from combining various resources in production.

Productivity

Efficiency of converting inputs into outputs, often reflected in the marginal product of labor.

Wage

Payment made to workers for their labor, forming the basis of variable costs in production.

Resource Constraint

Limitation imposed by fixed assets, such as ovens, restricting how much additional labor can boost output.

BackBack

BackBack

07:45

07:45