Skip to main content

Microeconomics

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

Back

Revenue, Cost, and Profit definitions

You can tap to flip the card.

Revenue

You can tap to flip the card.

👆

Revenue

Amount received from sales, representing the inflow of money to a firm, calculated as price times quantity sold.

Track progress

Control buttons has been changed to "navigation" mode.

1/17

Related flashcards

Related practice

Recommended videos

Revenue, Cost, and Profit quiz #1

Revenue, Cost, and Profit

14 Terms

Revenue, Cost, and Profit

10. The Costs of Production

10 problems

Topic

The Production Function and Diminishing Returns

10. The Costs of Production

10 problems

Topic

10. The Costs of Production

9 topics

15 problems

Chapter

Guided course

05:51

Explicit and Implicit Cost

5

views

Guided course

07:54

Fixed Costs and Variable Costs; Short Run and Long Run

4

views

Guided course

01:59

Accounting Profit and Economic Profit

4

views

Terms in this set (17)

Hide definitions

Revenue

Amount received from sales, representing the inflow of money to a firm, calculated as price times quantity sold.

Total Revenue

Sum of all money earned from sales, found by multiplying the selling price by the number of units sold.

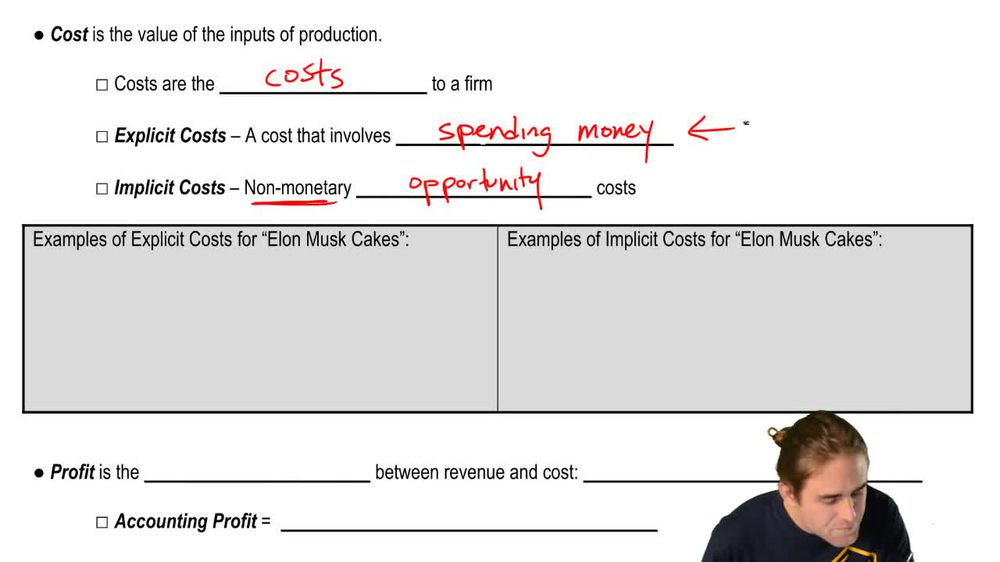

Cost

Value of inputs used in production, representing the outflow of resources necessary to create output.

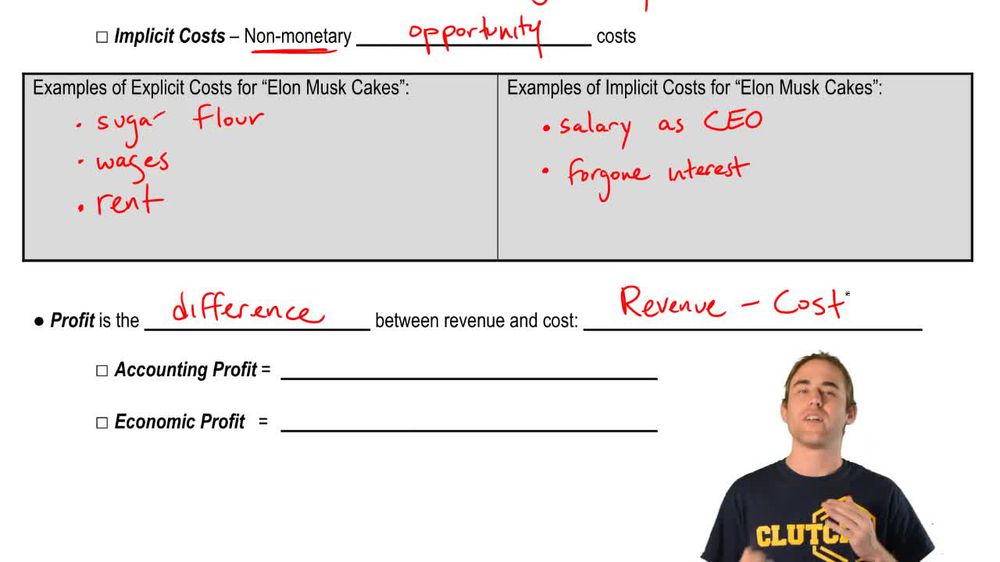

Explicit Cost

Direct monetary expenditure, such as wages or rent, easily observed as money leaving the firm.

Implicit Cost

Non-monetary opportunity cost, like foregone salary or interest, reflecting benefits sacrificed without cash payment.

Opportunity Cost

Value of the next best alternative forgone when a decision is made, including both monetary and non-monetary sacrifices.

Profit

Difference between revenue and cost, representing what remains after all expenses are subtracted from sales income.

Accounting Profit

Amount left after subtracting explicit costs from revenue, focusing only on direct monetary expenses.

Economic Profit

Amount left after subtracting both explicit and implicit costs from revenue, reflecting true opportunity costs.

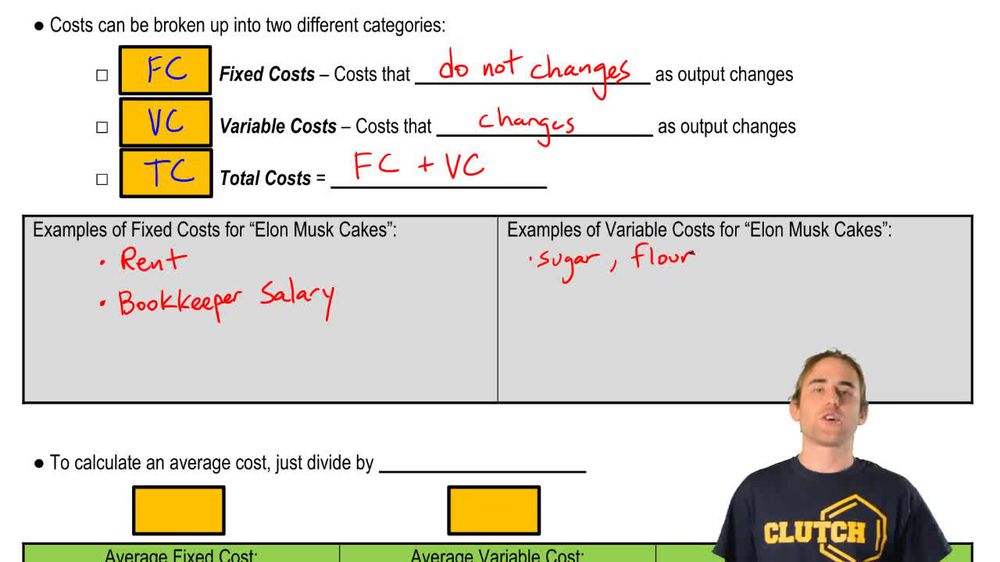

Fixed Cost

Expense that remains unchanged regardless of output level, such as rent or salaried employees.

Variable Cost

Expense that changes with output, including items like raw materials and day laborers.

Total Cost

Sum of fixed and variable costs, representing all expenses incurred in production.

Average Fixed Cost

Fixed cost per unit of output, calculated by dividing total fixed cost by the quantity produced.

Average Variable Cost

Variable cost per unit of output, found by dividing total variable cost by the number of units produced.

Average Total Cost

Total cost per unit, determined by dividing total cost by output or by adding average fixed and average variable costs.

Short Run

Time period in which at least one cost is fixed, limiting a firm's ability to adjust all inputs.

Long Run

Time period when all costs become variable, allowing full adjustment of business operations and inputs.

BackBack

BackBack

05:51

05:51