Skip to main content

Microeconomics

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

Back

Market Supply Curve in the Short Run and Long Run definitions

You can tap to flip the card.

Market Supply Curve

You can tap to flip the card.

👆

Market Supply Curve

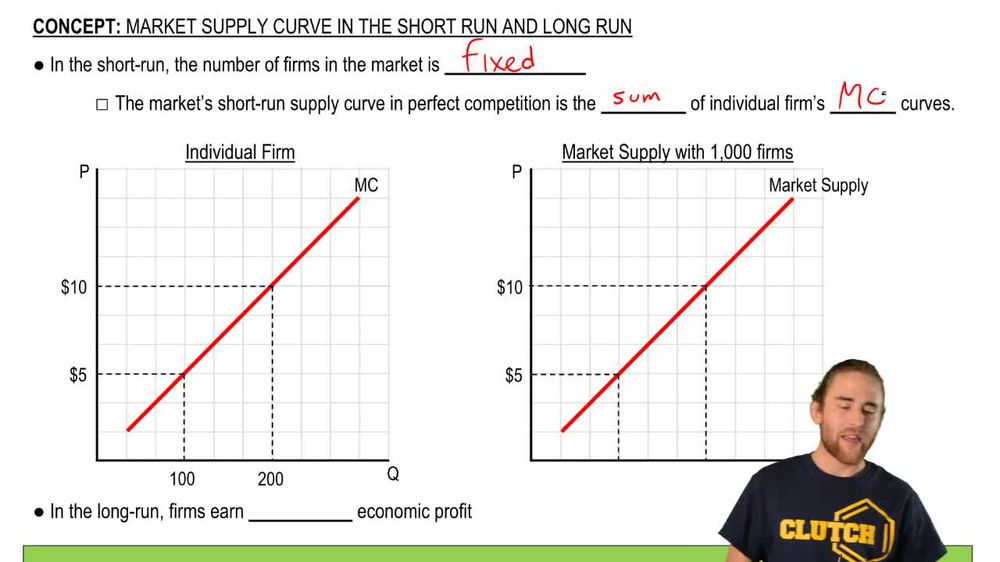

Represents total quantity supplied by all firms at each price, constructed by summing individual marginal cost curves.

Track progress

Control buttons has been changed to "navigation" mode.

1/15

Related flashcards

Related practice

Recommended videos

Market Supply Curve in the Short Run and Long Run quiz

Market Supply Curve in the Short Run and Long Run

15 Terms

Market Supply Curve in the Short Run and Long Run

11. Perfect Competition

10 problems

Topic

Long Run Equilibrium

11. Perfect Competition

10 problems

Topic

11. Perfect Competition

11 topics

15 problems

Chapter

Guided course

06:07

Market Supply Curve in the Long Run

3

views

Guided course

03:02

Market Supply Curve in the Short Run

4

views

Terms in this set (15)

Hide definitions

Market Supply Curve

Represents total quantity supplied by all firms at each price, constructed by summing individual marginal cost curves.

Short Run

Period where the number of firms is fixed, and market supply is determined by existing firms' marginal cost curves.

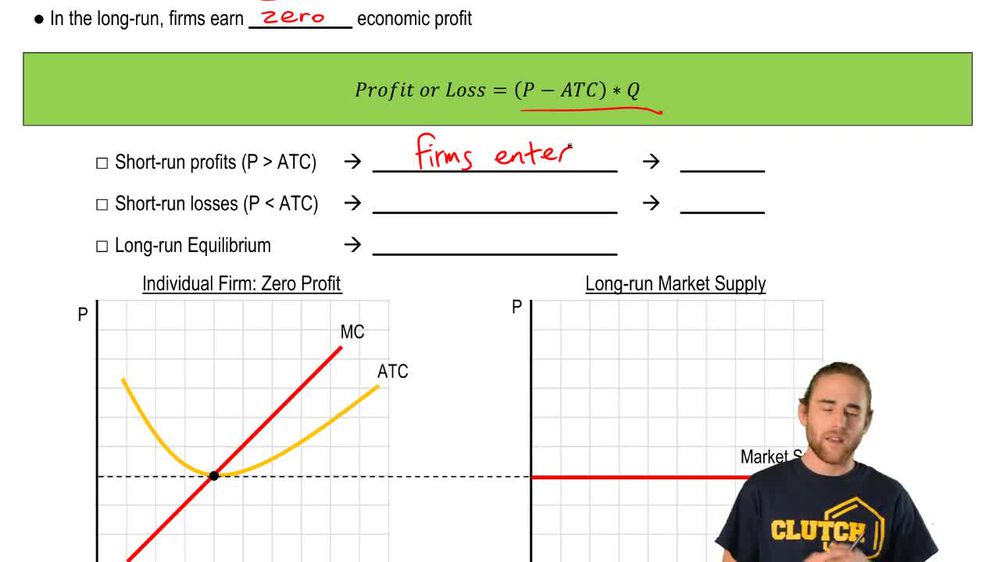

Long Run

Period allowing entry and exit of firms, leading to zero economic profit and a perfectly elastic supply curve.

Marginal Cost Curve

Graph showing the cost of producing one more unit, serving as the supply curve for individual firms above average variable cost.

Average Total Cost

Total cost per unit, including all fixed and variable costs, crucial for determining profit and market equilibrium.

Economic Profit

Profit calculation that includes opportunity costs, reaching zero in the long run due to market entry and exit.

Accounting Profit

Profit based solely on monetary costs and revenues, remaining positive even when economic profit is zero.

Opportunity Cost

Value of the next best alternative forgone, included in economic profit calculations for firms.

Equilibrium

State where market price equals average total cost, resulting in zero economic profit and stable firm numbers.

Perfectly Elastic Supply

Supply curve that is flat, indicating any quantity demanded can be supplied at a constant price in the long run.

Entry

Process where new firms join the market when profits exist, increasing supply and lowering price.

Exit

Process where firms leave the market when losses occur, reducing supply and raising price.

Minimum ATC

Lowest point on the average total cost curve, where firms produce efficiently and market price stabilizes.

Supply Shift

Movement of the supply curve due to changes in the number of firms, affecting market price and equilibrium.

Fixed Firms

Condition in the short run where the number of firms does not change, limiting supply adjustments.

BackBack

BackBack

06:07

06:07