Skip to main content

Microeconomics

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

Back

Individual Supply Curve in the Short Run and Long Run definitions

You can tap to flip the card.

Short Run

You can tap to flip the card.

👆

Short Run

A period during which a firm decides production based on covering variable costs, not all costs.

Track progress

Control buttons has been changed to "navigation" mode.

1/15

Related flashcards

Related practice

Recommended videos

Individual Supply Curve in the Short Run and Long Run quiz #1

Individual Supply Curve in the Short Run and Long Run

10 Terms

Individual Supply Curve in the Short Run and Long Run

11. Perfect Competition

10 problems

Topic

Market Supply Curve in the Short Run and Long Run

11. Perfect Competition

10 problems

Topic

11. Perfect Competition

11 topics

15 problems

Chapter

Guided course

03:12

Individual Firm Supply Curve in the Long Run

7

views

Guided course

03:19

Individual Firm Supply Curve in the Short Run

3

views

Terms in this set (15)

Hide definitions

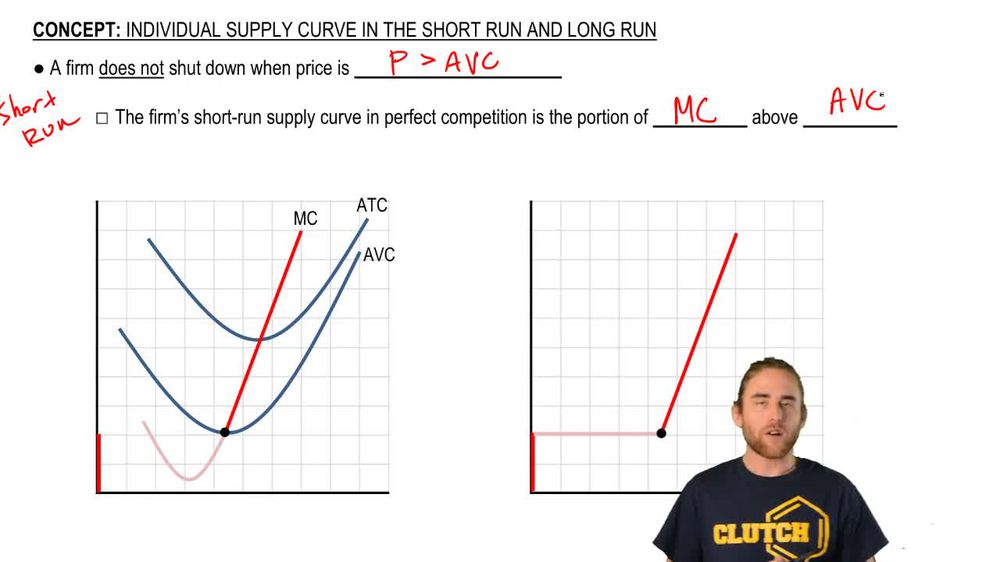

Short Run

A period during which a firm decides production based on covering variable costs, not all costs.

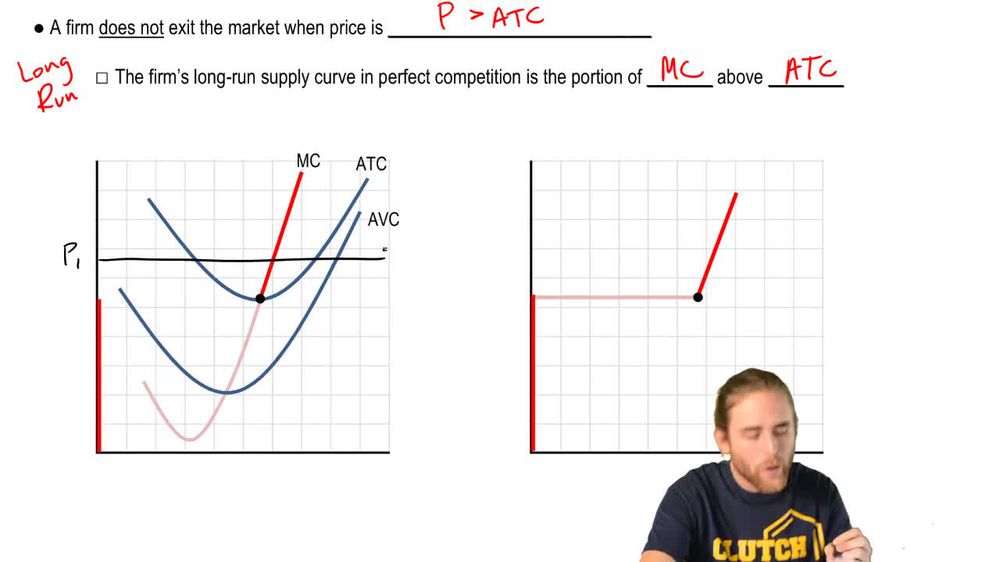

Long Run

A timeframe where a firm considers all costs and can exit or enter the market freely.

Average Variable Cost

The per-unit expense of variable inputs, crucial for determining production decisions in the short run.

Average Total Cost

The per-unit expense of all inputs, guiding a firm's market participation in the long run.

Marginal Cost

The extra expense incurred from producing one more unit, forming the basis of the supply curve.

Supply Curve

A graphical representation showing quantities a firm offers at various prices, shaped by cost conditions.

Perfect Competition

A market structure where firms are price takers and supply decisions depend on cost curves.

Shutdown Point

The price threshold below which a firm ceases production in the short run due to insufficient variable cost coverage.

Exit Point

The price threshold below which a firm leaves the market in the long run, not covering total costs.

Production Quantity

The amount a firm chooses to produce, determined by where revenue equals marginal cost above cost thresholds.

Minimum AVC

The lowest value of average variable cost, marking the start of the short run supply curve.

Minimum ATC

The lowest value of average total cost, marking the start of the long run supply curve.

Marginal Revenue

The additional income from selling one more unit, used to determine optimal production.

Profit

The surplus earned when price exceeds average total cost, motivating long run production.

Cost Curve

A graphical tool showing how costs change with output, essential for supply decisions.

BackBack

BackBack

03:12

03:12