Skip to main content

Microeconomics

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

Back

Four Market Model Summary: Perfect Competition quiz

You can tap to flip the card.

What is the number of firms like in a perfectly competitive market?

You can tap to flip the card.

👆

What is the number of firms like in a perfectly competitive market?

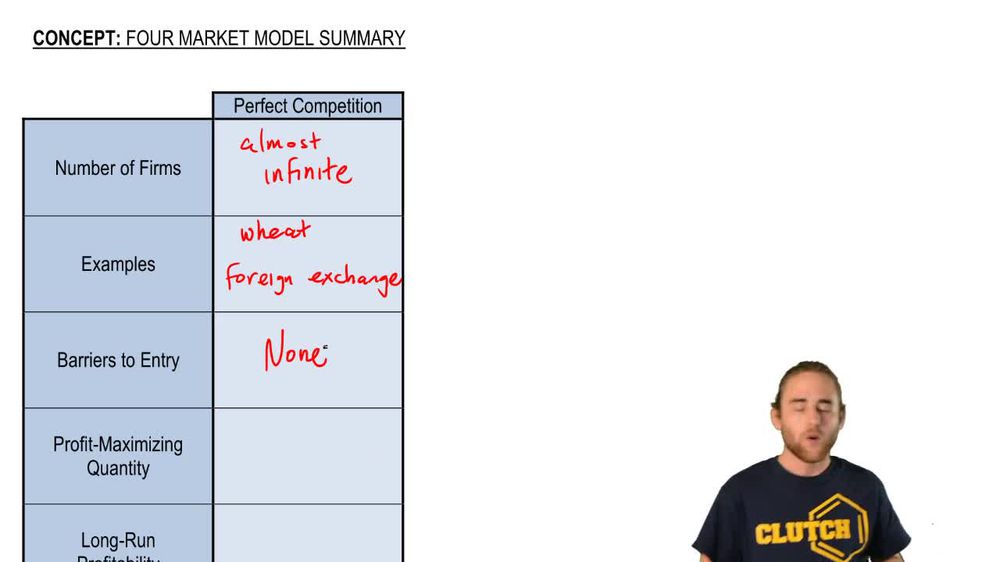

There are an almost infinite number of firms, so no single firm can influence the market price.

Track progress

Control buttons has been changed to "navigation" mode.

1/15

Related flashcards

Related practice

Recommended videos

Four Market Model Summary: Perfect Competition definitions

Four Market Model Summary: Perfect Competition

15 Terms

Four Market Model Summary: Perfect Competition

11. Perfect Competition

10 problems

Topic

Perfect Competition and Efficiency

11. Perfect Competition

10 problems

Topic

11. Perfect Competition

11 topics

15 problems

Chapter

Guided course

05:02

Four Market Model Summary: Perfect Competition

7

views

Terms in this set (15)

Hide definitions

What is the number of firms like in a perfectly competitive market?

There are an almost infinite number of firms, so no single firm can influence the market price.

Give two examples of markets that are often considered perfectly competitive.

Agricultural products like wheat and foreign exchange markets are examples of perfect competition.

What are barriers to entry, and do they exist in perfect competition?

Barriers to entry are obstacles that prevent new firms from entering a market, and in perfect competition, there are none.

How do firms in perfect competition maximize their profit?

Firms maximize profit where marginal revenue equals marginal cost.

What happens to economic profit for firms in perfect competition in the long run?

In the long run, firms in perfect competition cannot make economic profits; price stabilizes at the minimum of average total cost.

What is the relationship between price and average revenue in perfect competition?

In perfect competition, price always equals average revenue.

How does price relate to marginal revenue in perfect competition?

Price equals marginal revenue in perfect competition, which is unique among market structures.

What is the relationship between price and marginal cost in perfect competition?

Price equals marginal cost in perfect competition, leading to productive and allocative efficiency.

Why can't firms in perfect competition influence the market price?

Because each firm's output is a tiny fraction of the total market supply, so individual actions do not affect the overall price.

What does it mean for a market to have no barriers to entry or exit?

It means firms can freely enter or leave the market without facing obstacles.

At what point do firms in perfect competition choose their output level?

They choose the output where marginal revenue equals marginal cost.

What does it mean for price to be a 'flat line' in perfect competition?

It means the price remains constant regardless of the quantity produced by an individual firm.

What is the significance of price equaling marginal cost in perfect competition?

It ensures both productive and allocative efficiency in the market.

How does economic profit differ from accounting profit in perfect competition?

Economic profit includes opportunity costs, while accounting profit only considers explicit monetary costs.

Why is perfect competition considered efficient?

Because resources are allocated where price equals marginal cost, achieving both productive and allocative efficiency.

BackBack

BackBack

05:02

05:02