Skip to main content

Microeconomics

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

Back

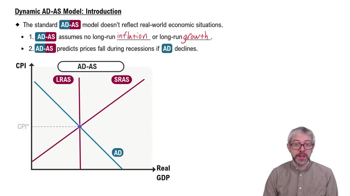

Dynamic AD-AS Model: Introduction definitions

You can tap to flip the card.

Dynamic AD-AS Model

You can tap to flip the card.

👆

Dynamic AD-AS Model

A framework where aggregate demand and supply curves shift over time, capturing real-world growth and inflation.

Track progress

Control buttons has been changed to "navigation" mode.

1/15

Related flashcards

Recommended videos

Dynamic AD-AS Model: Introduction quiz

Dynamic AD-AS Model: Introduction

15 Terms

04:59

Dynamic AD-AS Model: Introduction

Terms in this set (15)

Hide definitions

Dynamic AD-AS Model

A framework where aggregate demand and supply curves shift over time, capturing real-world growth and inflation.

Aggregate Demand

Total spending on goods and services in an economy, influenced by consumption, investment, and government expenditures.

Aggregate Supply

Total output producers are willing to supply at various price levels, affected by population and technology changes.

Long-Run Aggregate Supply

Represents potential GDP at full employment, shifting right as economies grow and technology advances.

Short-Run Aggregate Supply

Depicts current production capacity, moving right with population growth and technological improvements.

Potential GDP

Maximum sustainable output an economy can achieve when fully utilizing resources.

Equilibrium Price Level

The consumer price index where aggregate demand equals aggregate supply, marking macroeconomic balance.

Inflation

Persistent increase in overall price levels, common in most economies and overlooked in traditional models.

Economic Growth

Expansion of real GDP over time, driven by population increases and technological progress.

Consumer Price Index

A measure tracking changes in average prices paid by consumers for goods and services.

Recession

A period of declining economic activity, often misrepresented by traditional models as causing price drops.

Technological Advances

Improvements in production methods, enabling higher output and shifting supply curves rightward.

Population Growth

Increase in the number of people, leading to greater consumption and shifting demand and supply curves.

Investment

Expenditure by businesses to expand productive capacity, rising as economies grow.

Government Spending

Outlays by the public sector to provide services, increasing with population and economic expansion.

BackBack

BackBack

04:59

04:59