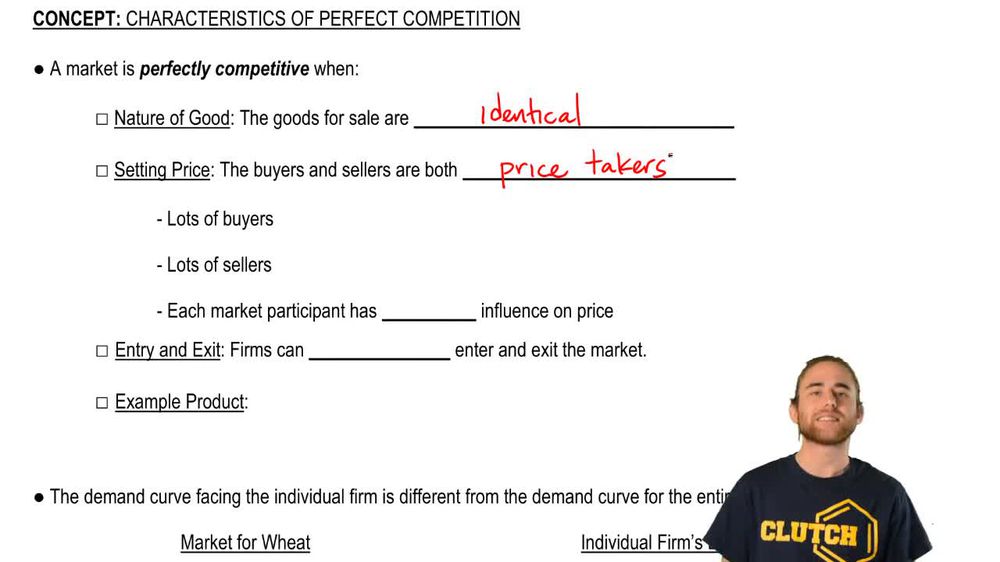

A market structure with identical goods, numerous buyers and sellers, and unrestricted entry and exit, resulting in participants having no control over price.

Identical Goods

Products that are indistinguishable from one another, making it impossible for buyers to differentiate between sellers based on product quality.

Price Taker

A participant who accepts the prevailing market price and cannot influence it by changing the quantity offered or demanded.

Free Entry

The ability for new firms to join the market without significant barriers, allowing anyone to start producing or selling.

Free Exit

The option for firms to leave the market at any time without facing prohibitive costs or restrictions.

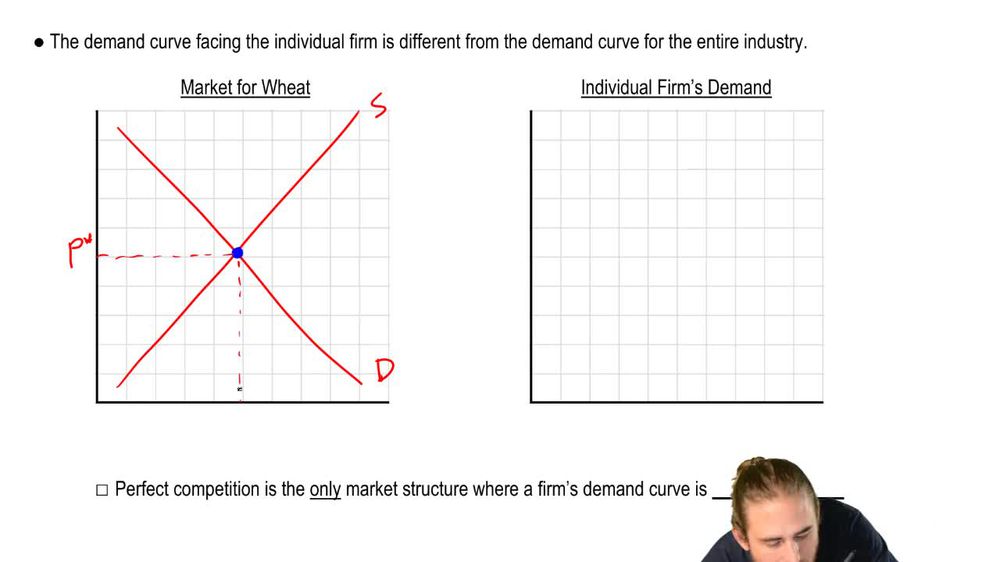

Market Demand Curve

A graphical representation showing the relationship between price and total quantity demanded by all buyers, typically downward sloping.

Market Supply Curve

A graphical representation showing the relationship between price and total quantity supplied by all sellers, typically upward sloping.

Equilibrium Price

The market-determined price where the quantity demanded equals the quantity supplied, ensuring all trades occur at this value.

Equilibrium Quantity

The amount of goods exchanged at the equilibrium price, where market supply and demand intersect.

Perfectly Elastic Demand

A demand curve that is horizontal, indicating a firm can sell any quantity at the market price but none above it.

Horizontal Demand Curve

A flat line representing a situation where the firm faces constant price regardless of output, unique to perfect competition.

Agricultural Product

A typical example of a perfectly competitive good, such as wheat, where products from different sellers are indistinguishable.

Foreign Exchange Market

A market where currencies are traded and each unit is identical, exemplifying perfect competition.

Back

Back

02:29

02:29