Skip to main content

Microeconomics

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

Back

AE Model: Algebraic Approach definitions

You can tap to flip the card.

Macroeconomic Equilibrium

You can tap to flip the card.

👆

Macroeconomic Equilibrium

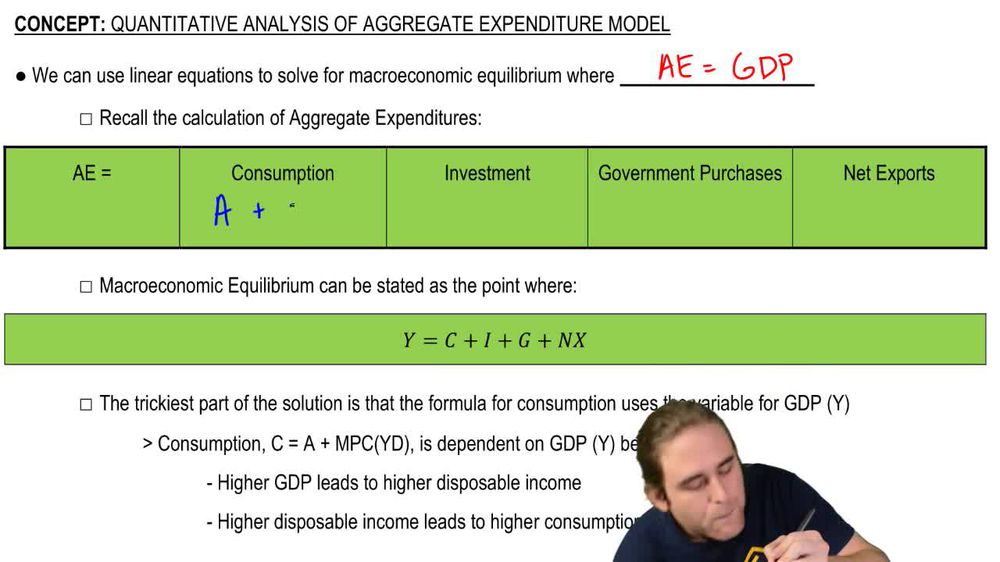

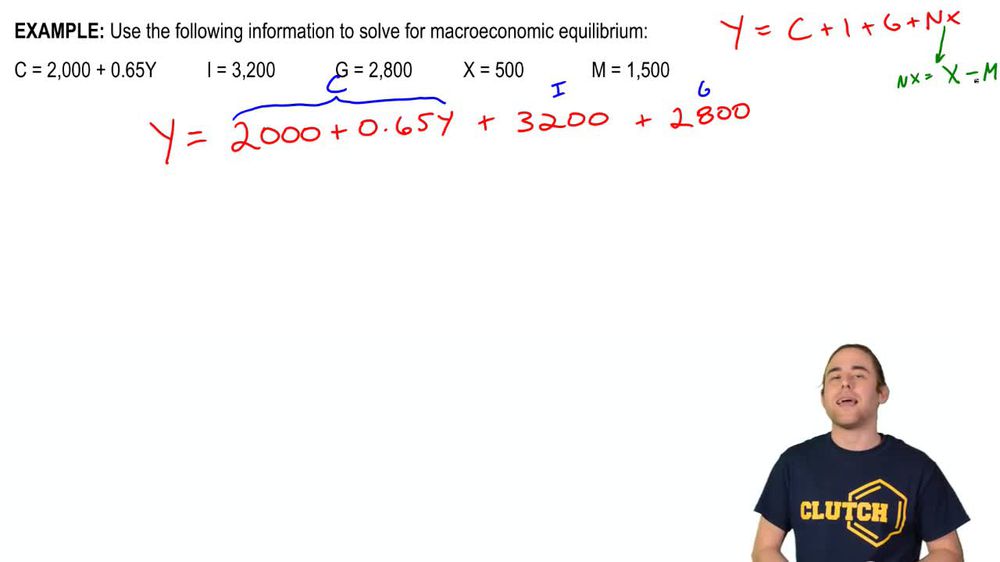

Occurs when total spending in the economy matches the value of goods and services produced, ensuring stability in output.

Track progress

Control buttons has been changed to "navigation" mode.

1/15

Related flashcards

Recommended videos

AE Model: Algebraic Approach quiz

AE Model: Algebraic Approach

15 Terms

Guided course

04:46

Aggregate Expenditures

1

views

Guided course

02:20

Algebraic Approach to the AE Model

1

views

Terms in this set (15)

Hide definitions

Macroeconomic Equilibrium

Occurs when total spending in the economy matches the value of goods and services produced, ensuring stability in output.

Aggregate Expenditures

Represents the sum of spending by households, businesses, government, and foreign buyers on goods and services.

Real GDP

Measures the total value of all final goods and services produced, adjusted for inflation, reflecting economic output.

Consumption

Refers to household spending on goods and services, influenced by income levels and economic conditions.

Disposable Income

Denotes the amount of income available to households after taxes, used for spending or saving.

Marginal Propensity to Consume

Indicates the fraction of additional income that households spend rather than save, shaping consumption patterns.

Market Equilibrium

Describes the point where supply and demand balance, resulting in stable prices and quantities.

Demand Curve

Illustrates the relationship between price and quantity demanded, typically sloping downward.

Economic Profits

Represents the surplus earned after accounting for all costs, including opportunity costs, in production.

Marginal Costs

Reflects the increase in total cost from producing one more unit of output, guiding production decisions.

Market Supply

Shows the total quantity of a good or service that producers are willing to offer at various prices.

Income

Signifies earnings from work, investments, or business, forming the basis for spending and saving.

Linear Equation

Expresses a straight-line relationship between variables, used to model economic interactions algebraically.

Base Consumption

Represents the minimum level of household spending, independent of income, in consumption models.

Aggregate Supply

Captures the total output of goods and services that producers are willing to supply at different price levels.

BackBack

BackBack

04:46

04:46