Skip to main content

Macroeconomics

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

Back

The Relationship Between Average Cost and Marginal Cost definitions

You can tap to flip the card.

Marginal Cost

You can tap to flip the card.

👆

Marginal Cost

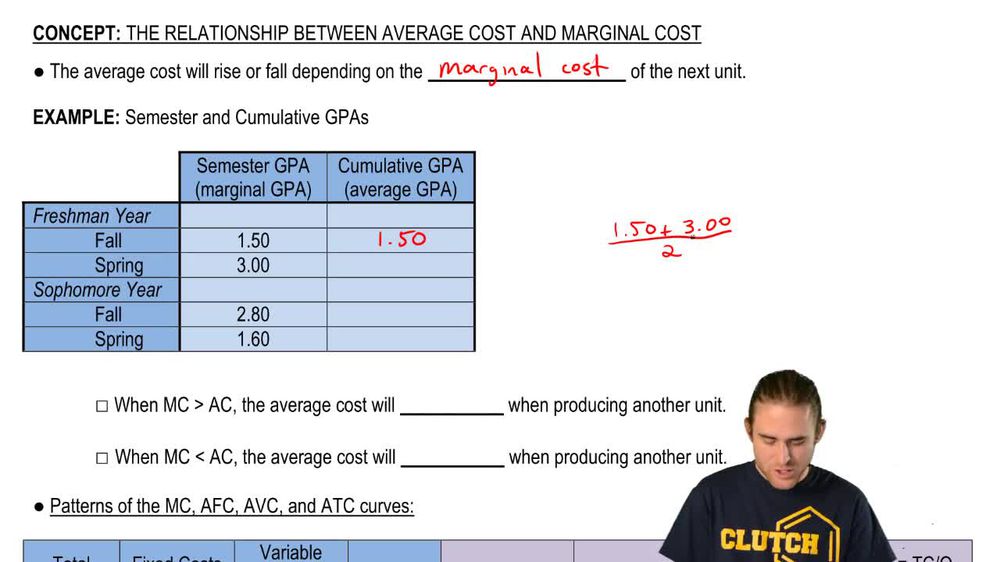

Change in total cost from producing one more unit, acting as the main driver for shifts in average cost.

Track progress

Control buttons has been changed to "navigation" mode.

1/14

Related flashcards

Recommended videos

The Relationship Between Average Cost and Marginal Cost quiz

The Relationship Between Average Cost and Marginal Cost

15 Terms

Guided course

08:56

Patterns of MC, AFC, AVC, and ATC curves

Guided course

06:38

Average Cost and Marginal Cost

Terms in this set (14)

Hide definitions

Marginal Cost

Change in total cost from producing one more unit, acting as the main driver for shifts in average cost.

Average Cost

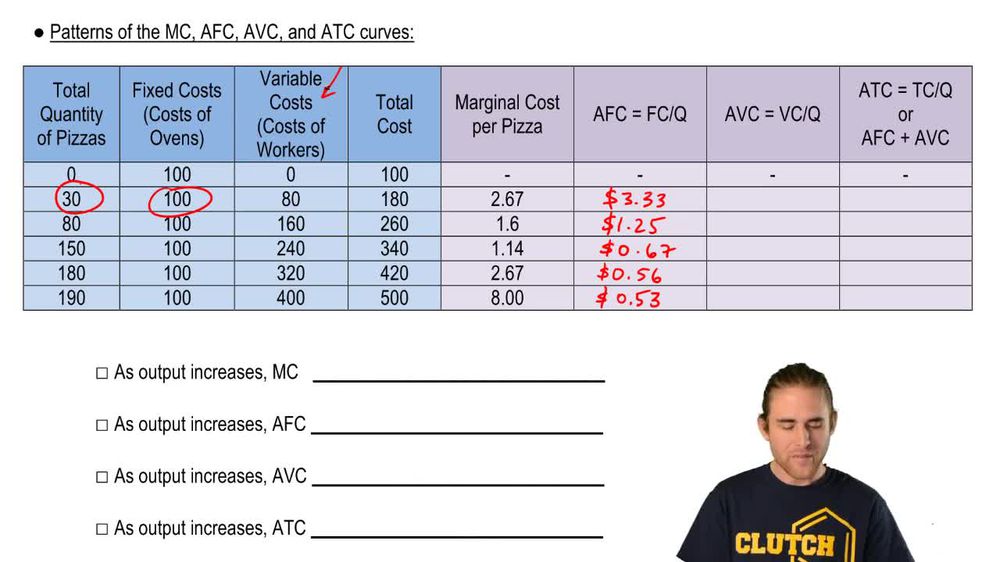

Total cost divided by output quantity, reflecting the per-unit expense of production.

Average Fixed Cost

Portion of cost that remains constant and is spread over increasing output, always declining as output rises.

Average Variable Cost

Per-unit expense from variable inputs, typically forming a U-shape as output increases.

Average Total Cost

Sum of per-unit fixed and variable expenses, showing a U-shaped pattern as output changes.

Fixed Cost

Expense that does not change with output, such as equipment or rent, impacting only the average fixed cost.

Variable Cost

Expense that rises with increased production, influencing both average variable and total costs.

Production Efficiency

Optimal use of resources to minimize per-unit expenses, highlighted by cost curve behaviors.

Cost Management

Strategic control of expenses to optimize output and profitability, informed by cost relationships.

Diminishing Marginal Productivity

Phenomenon where adding more input eventually yields smaller increases in output, affecting cost curves.

U-Shape

Characteristic pattern of average variable and total cost curves, falling then rising with output.

Aggregate Supply

Total output available in an economy, influenced by underlying cost structures and productivity.

Quantity

Number of units produced, serving as the denominator in average cost calculations.

Total Cost

Sum of all expenses, both fixed and variable, incurred in producing a given output.

BackBack

BackBack

08:56

08:56