Skip to main content

Macroeconomics

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

Back

Revenue, Cost, and Profit quiz

You can tap to flip the card.

How is total revenue calculated for a firm?

You can tap to flip the card.

👆

How is total revenue calculated for a firm?

Total revenue is calculated by multiplying the price per unit by the quantity of units sold.

Track progress

Control buttons has been changed to "navigation" mode.

1/15

Related flashcards

Recommended videos

Revenue, Cost, and Profit definitions

Revenue, Cost, and Profit

15 Terms

Guided course

01:59

Accounting Profit and Economic Profit

1

views

Guided course

05:51

Explicit and Implicit Cost

1

views

Guided course

07:54

Fixed Costs and Variable Costs; Short Run and Long Run

1

views

Terms in this set (15)

Hide definitions

How is total revenue calculated for a firm?

Total revenue is calculated by multiplying the price per unit by the quantity of units sold.

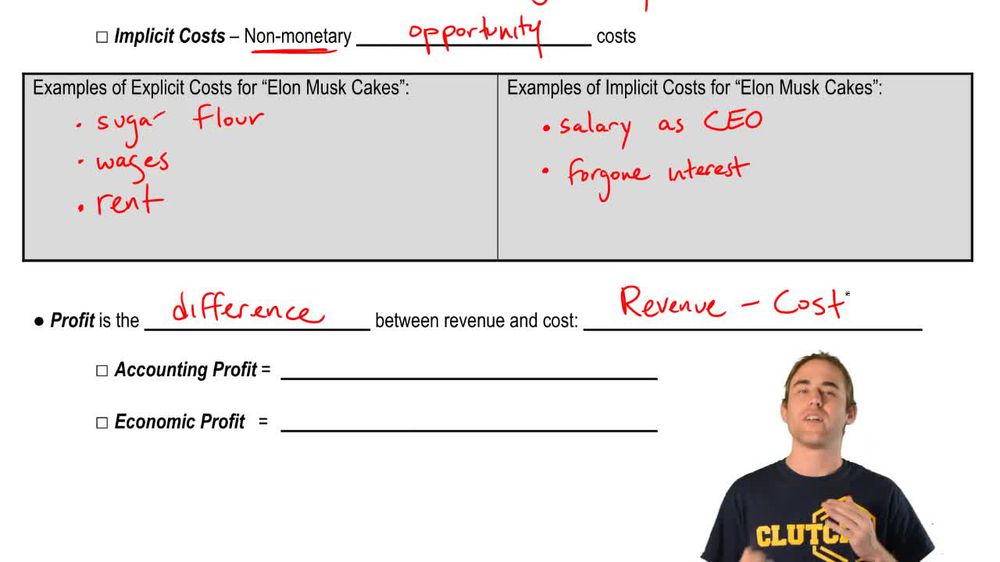

What is the difference between revenue and profit?

Revenue is the total money received from sales, while profit is what remains after subtracting costs from revenue.

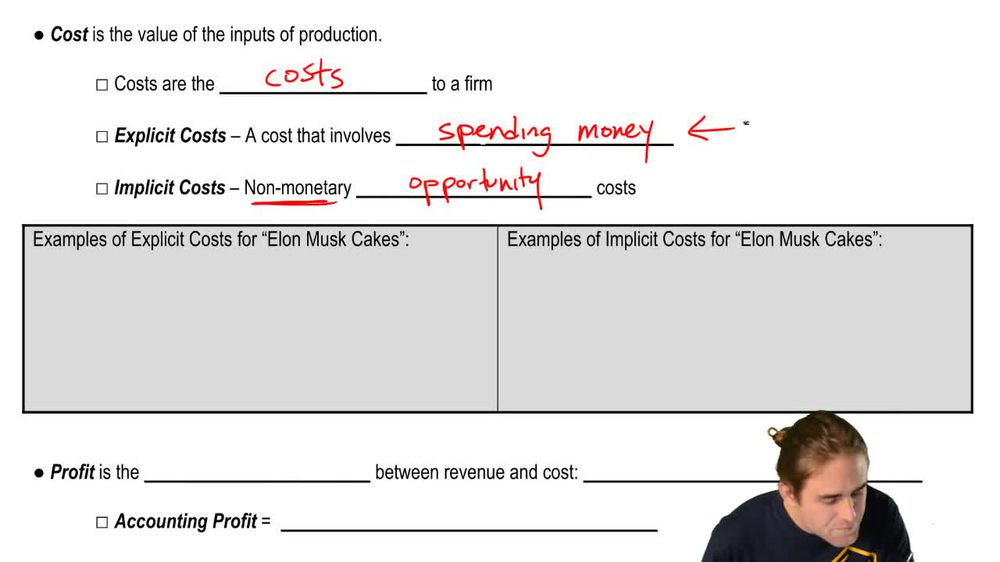

What is an explicit cost?

An explicit cost is a cost that involves a direct monetary payment, such as wages, rent, or materials.

What is an implicit cost?

An implicit cost is a non-monetary opportunity cost, such as foregone salary or interest, that does not involve a direct payment.

How do you calculate accounting profit?

Accounting profit is calculated as total revenue minus explicit costs.

How do you calculate economic profit?

Economic profit is calculated as total revenue minus both explicit and implicit costs.

Give an example of an explicit cost for a bakery.

Examples include paying for sugar, flour, employee wages, or rent for the bakery space.

Give an example of an implicit cost for a business owner.

An implicit cost could be the salary the owner gave up from a previous job or the interest lost by using savings to fund the business.

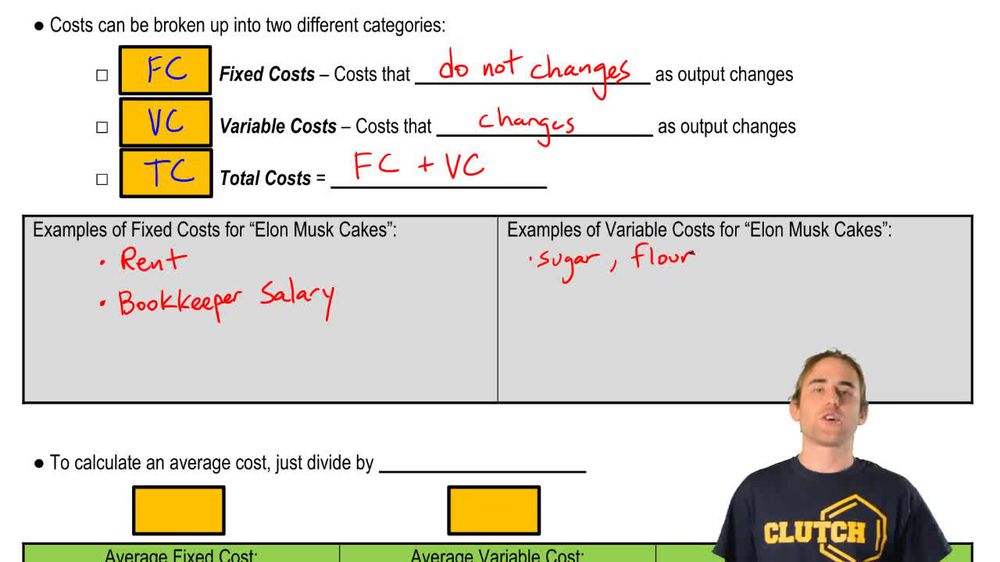

What is a fixed cost?

A fixed cost is a cost that does not change with the level of output, such as rent or a salaried employee's wage.

What is a variable cost?

A variable cost changes with the level of output, such as the cost of ingredients or hourly labor.

How do you calculate average fixed cost (AFC)?

Average fixed cost is calculated by dividing total fixed costs by the quantity of output produced.

How do you calculate average variable cost (AVC)?

Average variable cost is calculated by dividing total variable costs by the quantity of output produced.

How do you calculate average total cost (ATC)?

Average total cost is calculated by dividing total cost by quantity, or by adding average fixed cost and average variable cost.

What defines the short run in cost analysis?

The short run is a period in which at least one cost is fixed and cannot be changed.

What defines the long run in cost analysis?

The long run is a period in which all costs become variable, allowing the firm to adjust all inputs.

BackBack

BackBack

01:59

01:59