Skip to main content

Macroeconomics

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

Back

Antitrust Laws and Government Regulation of Monopolies definitions

You can tap to flip the card.

Antitrust Laws

You can tap to flip the card.

👆

Antitrust Laws

Legal measures designed to restrict market dominance and prevent practices that reduce competition among firms.

Track progress

Control buttons has been changed to "navigation" mode.

1/15

Related flashcards

Recommended videos

Antitrust Laws and Government Regulation of Monopolies quiz

Antitrust Laws and Government Regulation of Monopolies

15 Terms

Guided course

07:21

Monopoly:Socially Optimal Price and Fair-Return Price

1

views

Guided course

03:58

Antitrust Laws

1

views

Terms in this set (15)

Hide definitions

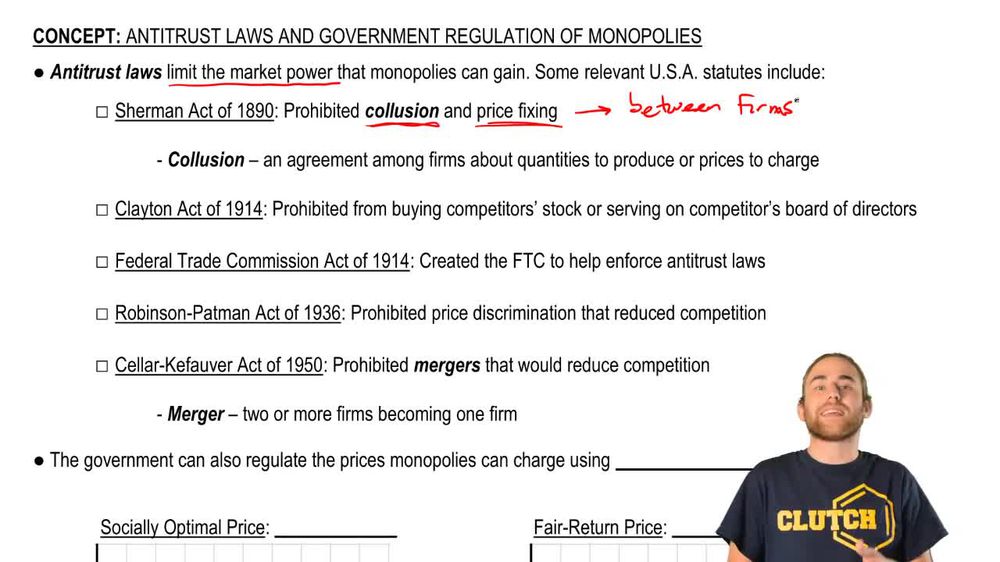

Antitrust Laws

Legal measures designed to restrict market dominance and prevent practices that reduce competition among firms.

Sherman Act

A foundational statute that prohibits agreements among firms to fix prices or collude, aiming to preserve market competition.

Clayton Act

Legislation that bans firms from acquiring competitors' stock or sharing board members to prevent anti-competitive consolidation.

Federal Trade Commission

A government agency responsible for enforcing competition laws and overseeing anti-competitive business practices.

Collusion

A secretive arrangement between firms to set prices or output, undermining competition and harming consumers.

Price Fixing

An agreement among competitors to set prices at a certain level, eliminating independent pricing and harming market fairness.

Price Discrimination

Charging different prices to various customers, which is only restricted when it significantly reduces competition.

Mergers

The combination of two firms, which may be blocked if it substantially decreases competition in the market.

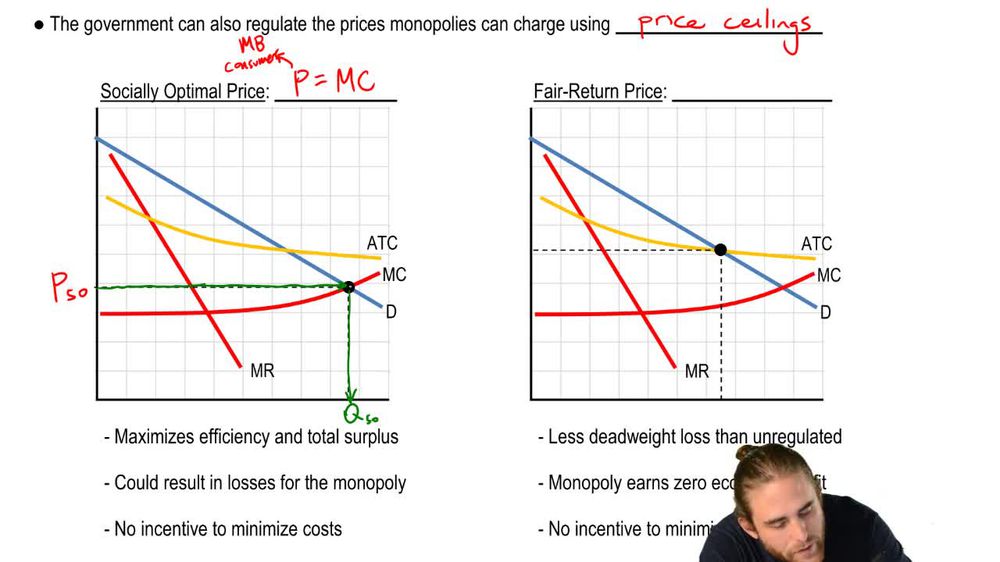

Price Ceiling

A regulatory cap on the maximum price a monopoly can charge, set to protect consumers and improve market outcomes.

Socially Optimal Price

A regulated price where consumer benefit equals production cost, maximizing efficiency but possibly causing firm losses.

Fair Return Price

A regulated price set at the firm's average total cost, ensuring no profit but allowing cost coverage and continued operation.

Deadweight Loss

The loss of total surplus due to unmade trades, often resulting from monopolistic pricing or imperfect regulation.

Allocative Efficiency

A market state where resources are distributed so that consumer benefit matches production cost for the last unit.

Productive Efficiency

A condition where goods are produced at the lowest possible cost, typically achieved when price equals average total cost.

Market Power

The ability of a firm to influence prices and output levels, often leading to reduced competition and higher profits.

BackBack

BackBack

07:21

07:21