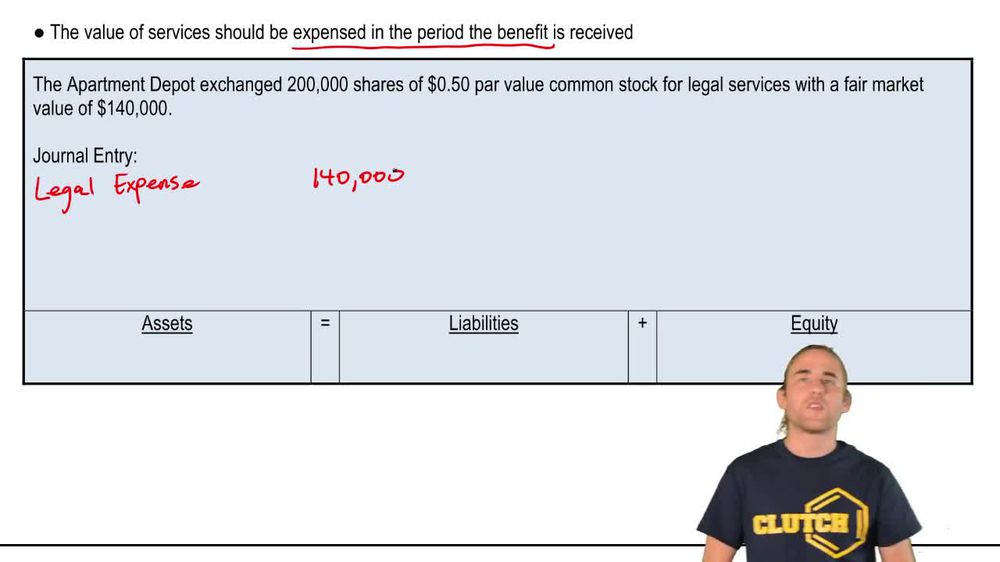

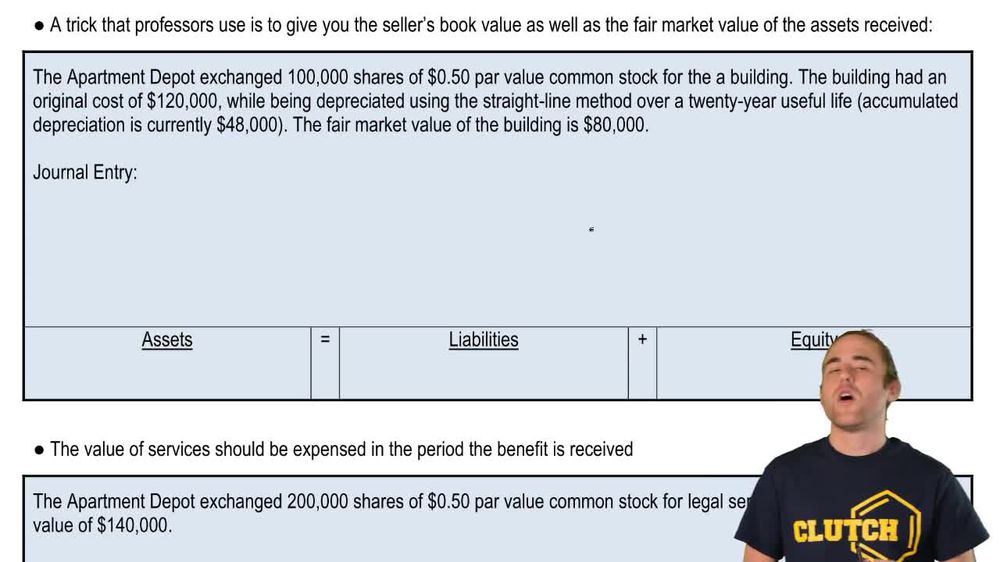

How should a company record the issuance of common stock in exchange for a non-cash asset, such as a building, and what values are used in the journal entry?

When a company issues common stock for a non-cash asset, the asset is recorded at its fair market value. The journal entry debits the asset account for the fair market value, credits common stock for the par value of the shares issued, and credits additional paid-in capital (APIC) for the excess of the asset's value over the par value.

Back

Back

05:37

05:37