Skip to main content

Financial Accounting

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

Back

GAAP vs. IFRS: Stockholders' Equity definitions

You can tap to flip the card.

GAAP

You can tap to flip the card.

👆

GAAP

A set of accounting rules established by FASB, primarily used in the United States for financial reporting.

Track progress

Control buttons has been changed to "navigation" mode.

1/15

Related flashcards

Related practice

Recommended videos

GAAP vs. IFRS: Stockholders' Equity quiz

GAAP vs. IFRS: Stockholders' Equity

15 Terms

GAAP vs. IFRS: Stockholders' Equity

15. GAAP vs IFRS

10 problems

Topic

GAAP vs. IFRS: Statement of Cash Flows

15. GAAP vs IFRS

10 problems

Topic

15. GAAP vs IFRS

13 topics

13 problems

Chapter

Guided course

03:39

GAAP vs. IFRS: Stockholders' Equity

3

views

Terms in this set (15)

Hide definitions

GAAP

A set of accounting rules established by FASB, primarily used in the United States for financial reporting.

IFRS

International accounting standards developed by the IASB, used globally for financial statement preparation.

FASB

The U.S. organization responsible for creating and updating generally accepted accounting principles.

IASB

The international body that develops and issues International Financial Reporting Standards.

Stockholders' Equity

The residual interest in a company's assets after deducting liabilities, including paid-in capital and retained earnings.

Paid-in Capital

Funds contributed by shareholders through the purchase of stock, including common and preferred shares.

Treasury Stock

Shares that were issued and later reacquired by the company, reducing total stockholders' equity.

Retained Earnings

Accumulated net income not distributed as dividends, often included in reserves under IFRS.

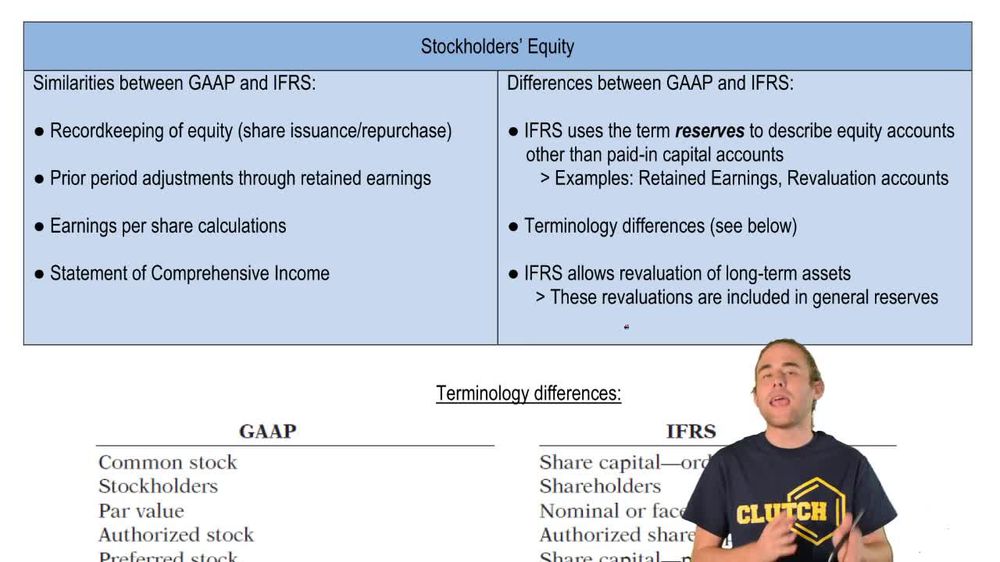

Reserves

Under IFRS, items in equity not classified as paid-in capital, such as retained earnings and revaluation accounts.

Revaluation Accounts

Equity accounts under IFRS reflecting adjustments from revaluing long-term assets.

Comprehensive Income

Total change in equity from net income and other complex items not included in net income.

Net Income

The profit remaining after all expenses, taxes, and costs are subtracted from total revenue.

Earnings Per Share

A financial metric showing the portion of a company's profit allocated to each outstanding share.

Prior Period Adjustments

Corrections to previously issued financial statements, typically affecting retained earnings.

Change in Accounting Principle

A switch in accounting methods, such as from weighted average to FIFO, requiring retroactive adjustments.

BackBack

BackBack

03:39

03:39