Skip to main content

Financial Accounting

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

Back

GAAP vs. IFRS: Long Lived Assets quiz

You can tap to flip the card.

What does GAAP stand for and who sets its standards?

You can tap to flip the card.

👆

What does GAAP stand for and who sets its standards?

GAAP stands for Generally Accepted Accounting Principles, and its standards are set by the Financial Accounting Standards Board (FASB).

Track progress

Control buttons has been changed to "navigation" mode.

1/15

Related flashcards

Related practice

Recommended videos

GAAP vs. IFRS: Long Lived Assets definitions

GAAP vs. IFRS: Long Lived Assets

15 Terms

GAAP vs. IFRS: Long Lived Assets

15. GAAP vs IFRS

10 problems

Topic

GAAP vs. IFRS: Liabilities

15. GAAP vs IFRS

9 problems

Topic

15. GAAP vs IFRS

13 topics

13 problems

Chapter

Guided course

05:02

GAAP vs. IFRS: Long-Lived Assets

1

views

Terms in this set (15)

Hide definitions

What does GAAP stand for and who sets its standards?

GAAP stands for Generally Accepted Accounting Principles, and its standards are set by the Financial Accounting Standards Board (FASB).

What does IFRS stand for and who sets its standards?

IFRS stands for International Financial Reporting Standards, and its standards are set by the International Accounting Board.

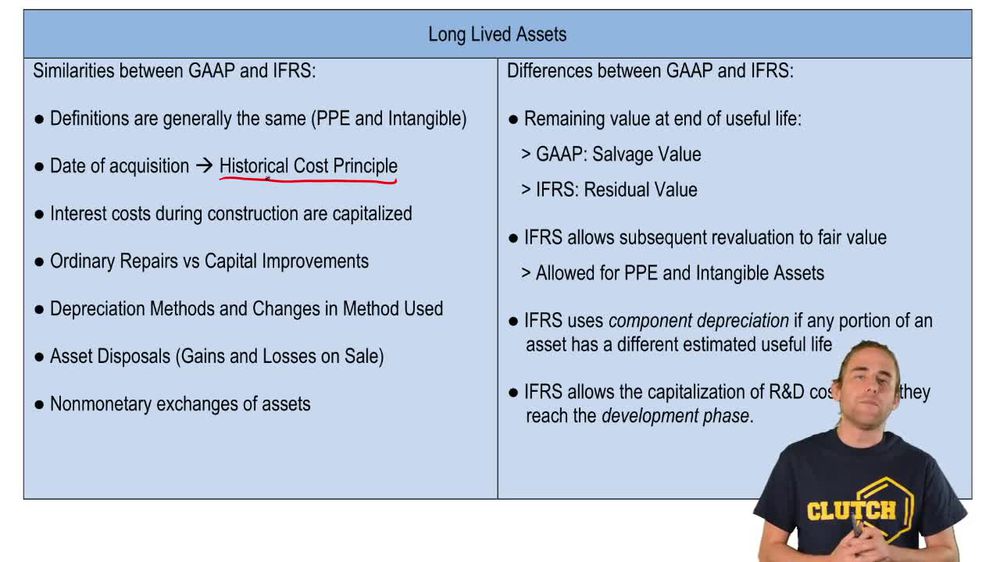

How do GAAP and IFRS define long-lived assets?

Both GAAP and IFRS define long-lived assets as including property, plant, equipment, and intangibles.

What principle is used for asset acquisition under both GAAP and IFRS?

The historical cost principle is used for asset acquisition under both GAAP and IFRS.

How are ordinary repairs treated under GAAP and IFRS?

Ordinary repairs are expensed under both GAAP and IFRS.

How are capital improvements treated under GAAP and IFRS?

Capital improvements are capitalized as assets under both GAAP and IFRS.

What are the common depreciation methods used under GAAP and IFRS?

Both GAAP and IFRS use straight line, double declining, and units of activity depreciation methods.

What term does GAAP use for the remaining value of an asset at the end of its useful life?

GAAP uses the term 'salvage value' for the remaining value of an asset.

What term does IFRS use for the remaining value of an asset at the end of its useful life?

IFRS uses the term 'residual value' for the remaining value of an asset.

Can assets be revalued to fair value under IFRS?

Yes, IFRS allows subsequent revaluation of assets to fair value.

Does GAAP allow subsequent revaluation of assets to fair value?

No, GAAP does not allow subsequent revaluation of assets to fair value.

What is component depreciation and which standard allows it?

Component depreciation is depreciating parts of an asset with different useful lives separately, and it is allowed under IFRS.

How does GAAP treat component depreciation?

GAAP does not have specific rules about component depreciation.

How are research and development (R&D) costs treated under GAAP?

Under GAAP, research and development costs are always expensed.

How are research and development (R&D) costs treated under IFRS?

Under IFRS, R&D costs can be capitalized once the development phase is reached.

BackBack

BackBack

05:02

05:02