GAAP is created by the Financial Accounting Standards Board (FASB) and is primarily used in the United States.

Who is responsible for developing IFRS and where is it applied?

The International Accounting Standards Board (IASB) develops IFRS, which is used internationally.

Are financial analysis tools like horizontal and vertical analysis specific to GAAP or IFRS?

No, these tools are globally applicable and not specific to either GAAP or IFRS.

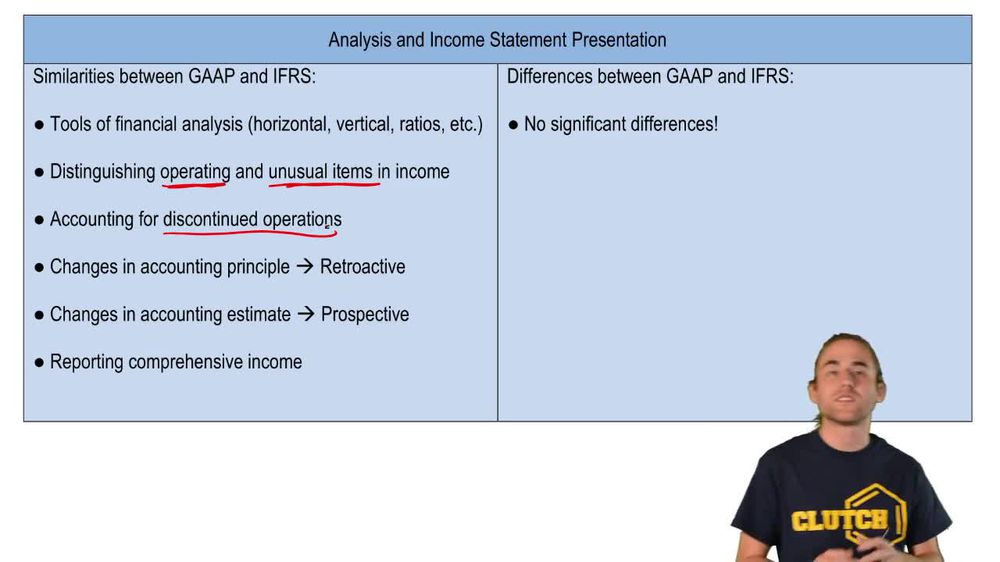

How do GAAP and IFRS treat operating and unusual items?

Both GAAP and IFRS treat operating and unusual items similarly, ensuring consistent accounting for non-routine transactions.

How must discontinued operations be reported under GAAP and IFRS?

Discontinued operations must be reported separately from ongoing operations under both GAAP and IFRS.

What is required when there is a change in accounting principle under GAAP and IFRS?

A change in accounting principle requires retroactive restatement under both GAAP and IFRS.

How are changes in accounting estimates handled under GAAP and IFRS?

Changes in accounting estimates are handled prospectively, meaning only future statements are affected.

What is comprehensive income and how is it treated under GAAP and IFRS?

Comprehensive income includes net income plus other items like unrealized gains and losses, and is treated similarly under both GAAP and IFRS.

What is a key difference in the approach of GAAP compared to IFRS?

GAAP is more rules-based, providing strict guidelines, while IFRS is more principles-based, allowing more professional judgment.

How does IFRS differ from GAAP regarding the revaluation of long-term assets?

IFRS allows the revaluation of long-term assets, whereas GAAP generally does not.

Is the LIFO inventory valuation method permitted under IFRS?

No, IFRS prohibits the use of the LIFO (Last In, First Out) inventory valuation method.

Do GAAP and IFRS differ significantly in the presentation of the income statement?

No, there are no significant differences in the analysis and presentation of the income statement between GAAP and IFRS.

What is an example of an unusual item that must be accounted for under both GAAP and IFRS?

An example is the sale of a piece of factory equipment, which is not a routine transaction.

When a company stops a portion of its business, how is this shown in financial statements under GAAP and IFRS?

It is shown as discontinued operations, reported separately from continuing operations.

What are the three main differences between GAAP and IFRS highlighted in the lesson?

The three main differences are: GAAP is rules-based while IFRS is principles-based, IFRS allows revaluation of long-term assets, and IFRS does not allow LIFO for inventory.

Back

Back

05:09

05:09