Skip to main content

Financial Accounting

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

Back

GAAP vs. IFRS: Adjusting Entries quiz

You can tap to flip the card.

Who sets GAAP and what region does it apply to?

You can tap to flip the card.

👆

Who sets GAAP and what region does it apply to?

GAAP is set by the Financial Accounting Standards Board (FASB) and applies to the United States.

Track progress

Control buttons has been changed to "navigation" mode.

1/15

Related flashcards

Related practice

Recommended videos

GAAP vs. IFRS: Adjusting Entries definitions

GAAP vs. IFRS: Adjusting Entries

15 Terms

GAAP vs. IFRS: Adjusting Entries

15. GAAP vs IFRS

10 problems

Topic

GAAP vs. IFRS: Merchandising

15. GAAP vs IFRS

10 problems

Topic

15. GAAP vs IFRS

13 topics

13 problems

Chapter

Guided course

04:03

GAAP vs. IFRS: Adjusting Entries

2

views

Terms in this set (15)

Hide definitions

Who sets GAAP and what region does it apply to?

GAAP is set by the Financial Accounting Standards Board (FASB) and applies to the United States.

Who sets IFRS and where is it used?

IFRS is set by the International Accounting Standards Board and is used internationally.

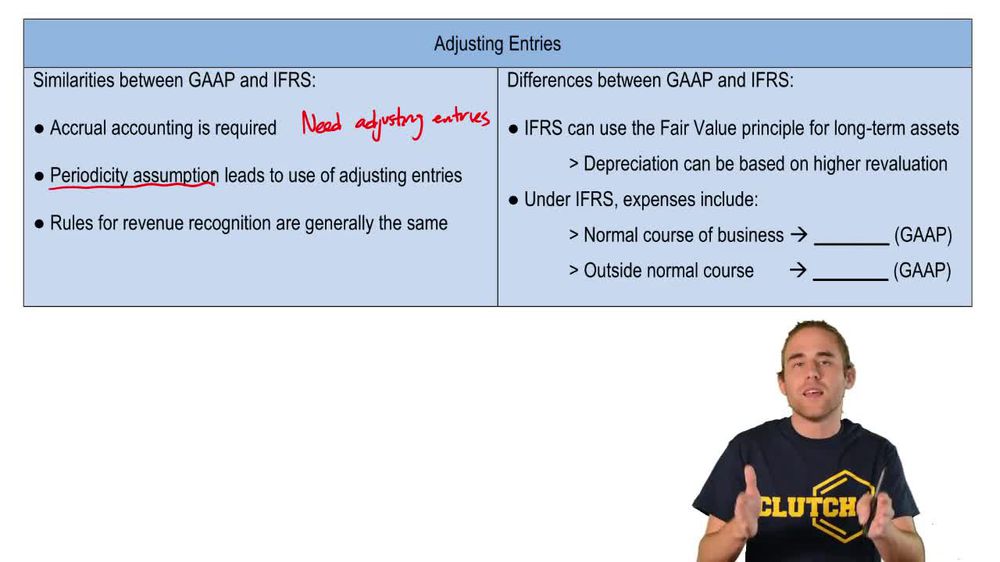

What type of accounting is required under both GAAP and IFRS?

Both GAAP and IFRS require accrual accounting.

What is the Periodicity Assumption in accounting?

The Periodicity Assumption involves breaking up an indefinite timeline into artificial time periods, usually a year, for financial reporting.

Why are adjusting entries necessary in accrual accounting?

Adjusting entries are necessary to properly record revenues and expenses in the correct time periods under accrual accounting.

Are revenue recognition rules the same under GAAP and IFRS?

Yes, the revenue recognition rules discussed in the course are generally the same under both GAAP and IFRS.

What principle does IFRS use that can affect asset valuation?

IFRS uses the fair value principle, which can change the value of long-term assets.

How does the fair value principle under IFRS impact depreciation calculations?

Revaluation of assets under IFRS can change depreciation calculations based on the updated asset value.

Does GAAP allow revaluation of long-term assets?

No, GAAP does not allow revaluation of long-term assets, making depreciation calculations simpler.

Are the methods for calculating depreciation generally the same under GAAP and IFRS?

Yes, the methods for calculating depreciation are generally the same, but IFRS may adjust asset values.

How does GAAP classify losses outside the normal course of business?

GAAP classifies losses outside the normal course of business as 'losses.'

How does IFRS classify losses outside the normal course of business?

IFRS categorizes losses outside the normal course of business as 'expenses.'

What is a key terminology difference between GAAP and IFRS regarding losses?

GAAP uses 'losses' for events outside normal business, while IFRS uses 'expenses' for similar events.

What is the main focus of adjusting entries in both GAAP and IFRS?

The main focus is to ensure revenues and expenses are recorded in the correct time periods.

Do businesses stop operations for financial reporting under the Periodicity Assumption?

No, businesses continue operating, but financial reporting is done for artificial time periods.

BackBack

BackBack

04:03

04:03