Skip to main content

Financial Accounting

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

Back

Exchange for Similar Assets quiz

You can tap to flip the card.

What is meant by 'exchange for similar fixed assets' in accounting?

You can tap to flip the card.

👆

What is meant by 'exchange for similar fixed assets' in accounting?

It refers to trading in an old fixed asset, like a truck, for a new one of a similar type, often involving a trade-in value.

Track progress

Control buttons has been changed to "navigation" mode.

1/15

Related flashcards

Related practice

Recommended videos

Exchange for Similar Assets definitions

Exchange for Similar Assets

15 Terms

Exchange for Similar Assets

8. Long Lived Assets

10 problems

Topic

Asset Impairments

8. Long Lived Assets

9 problems

Topic

8. Long Lived Assets - Part 1 of 2

14 topics

15 problems

Chapter

8. Long Lived Assets - Part 2 of 2

1 topic

3 problems

Chapter

Guided course

11:54

Asset Exchanges

3

views

Terms in this set (15)

Hide definitions

What is meant by 'exchange for similar fixed assets' in accounting?

It refers to trading in an old fixed asset, like a truck, for a new one of a similar type, often involving a trade-in value.

How is 'trade-in value' defined in the context of asset exchanges?

Trade-in value is the amount offered by the dealer for the old asset, which may be more or less than its net book value.

What does the term 'boot' refer to in an asset exchange?

'Boot' is any additional cash paid or received in the transaction, beyond the value of the asset exchanged.

What is 'commercial substance' in an exchange transaction?

Commercial substance means the exchange will result in changes to future cash flows for the company.

How do you calculate the net book value of an old asset?

Net book value is calculated by subtracting accumulated depreciation from the asset's original cost.

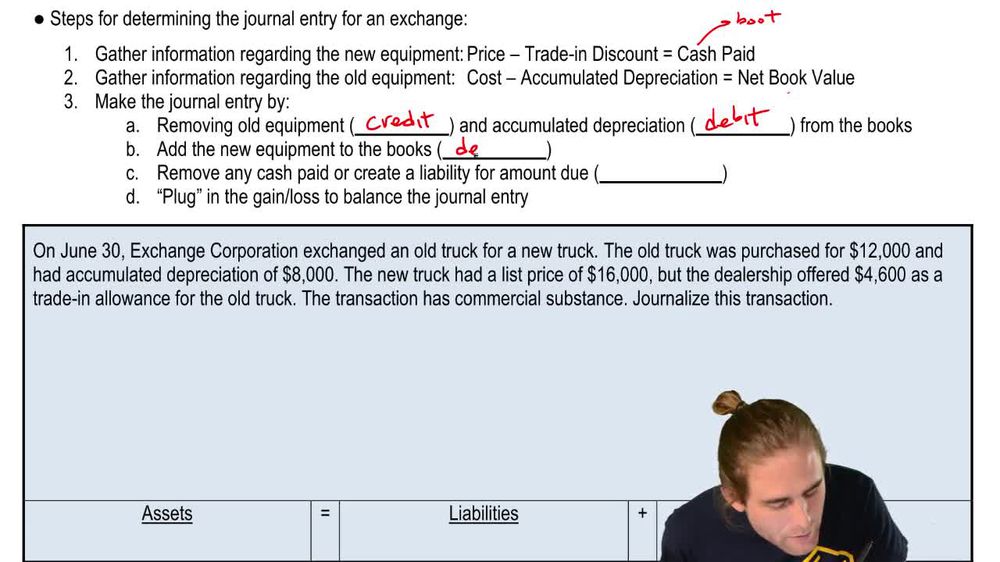

What is the first step in accounting for an exchange of similar assets?

The first step is to determine the price of the new equipment minus any trade-in discount.

How do you remove the old equipment from the books during an exchange?

You credit the old equipment account for its original cost and debit accumulated depreciation for its total amount.

How is the new equipment recorded in the journal entry?

The new equipment is added to the books with a debit for its full price.

What do you do with any cash paid in the exchange?

Any cash paid is credited to the cash account, reflecting the outflow of cash.

How do you determine if there is a gain or loss on the exchange?

A gain or loss is calculated as the difference between the trade-in value received and the net book value of the old asset.

In the example, what was the net book value of the old truck?

The net book value was \$4,000, calculated as the \$12,000 cost minus \$8,000 accumulated depreciation.

What was the trade-in allowance given for the old truck in the example?

The trade-in allowance was \$4,600.

How much cash was paid for the new truck after the trade-in allowance?

The cash paid was \$11,400, which is the \$16,000 price minus the \$4,600 trade-in allowance.

What was the gain recognized on the exchange in the example?

A gain of \(600 was recognized, as the trade-in value exceeded the net book value by \)600.

How does the gain on exchange affect the company's equity?

The gain increases the company's equity by the amount of the gain recognized.

BackBack

BackBack

11:54

11:54