What determines whether a bond is issued at a premium or a discount?

A bond is issued at a premium if the stated rate is higher than the market rate, and at a discount if the stated rate is lower than the market rate.

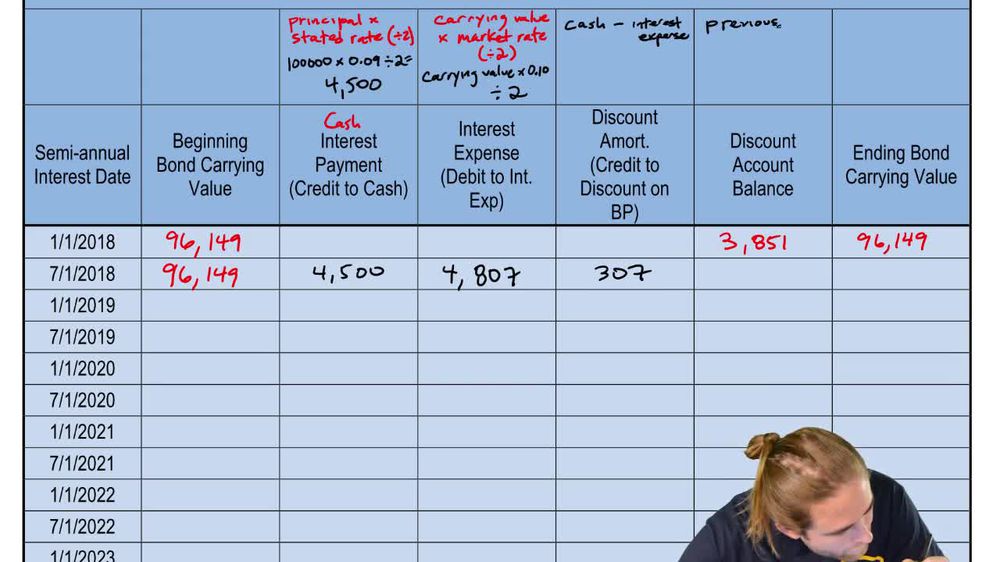

How do you calculate the price of a bond using present value tables?

Calculate the present value of future interest payments (an annuity) and the principal payment (lump sum), then add them together.

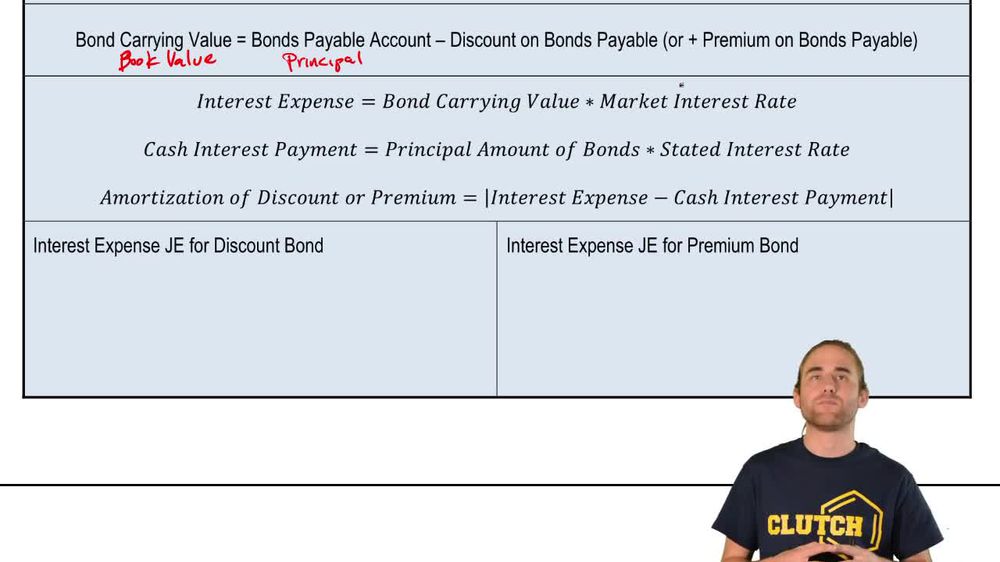

What is the carrying value of a bond?

The carrying value is the principal amount minus any discount or plus any premium, representing the bond's book value.

How is cash interest payment calculated for a bond?

Cash interest payment is the principal amount multiplied by the stated interest rate, divided by the number of periods if payments are not annual.

What formula is used to calculate interest expense under the effective interest method?

Interest expense is calculated as the carrying value of the bond multiplied by the market interest rate, adjusted for the payment period.

How is the amortization of a bond discount or premium determined?

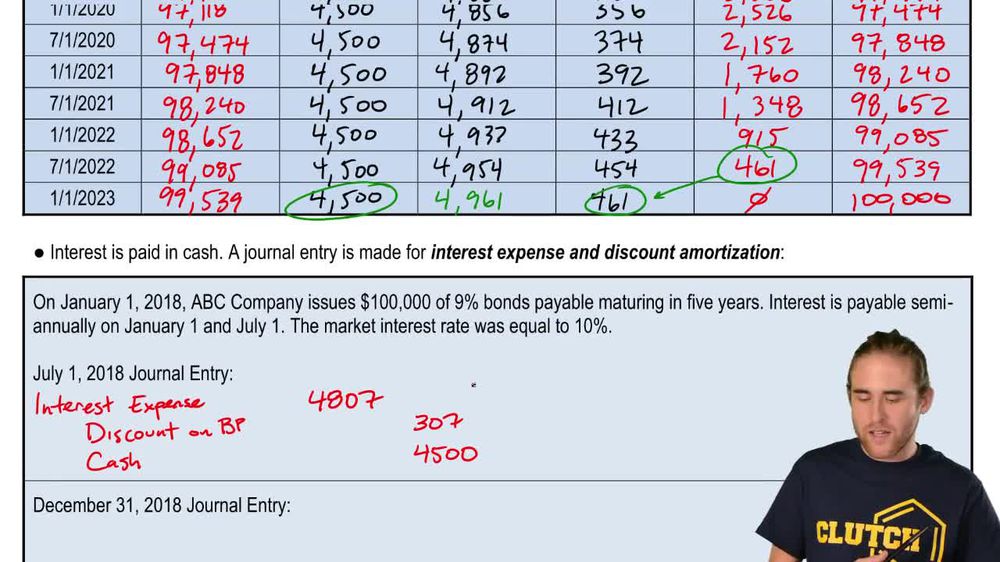

Amortization is the difference between the interest expense and the cash interest payment for each period.

What stays constant in the effective interest amortization table for a bond?

The cash interest payment remains constant because it is based on the principal and stated rate.

How does the carrying value of a discounted bond change over time?

The carrying value increases each period as the discount is amortized, eventually reaching the face value at maturity.

What are the three parts of the journal entry for interest expense under the effective interest method?

The journal entry includes a debit to interest expense, a credit to cash (or interest payable), and an adjustment for the discount or premium.

How is the discount on bonds payable account updated each period?

The discount account balance is reduced by the amount of discount amortization for the period.

What happens to the discount or premium account at bond maturity?

At maturity, the discount or premium account is fully amortized, and the carrying value equals the face value of the bond.

Why does the interest expense change each period under the effective interest method?

Interest expense changes because it is based on the changing carrying value of the bond, not the original principal.

What is the purpose of the amortization table in bond accounting?

The amortization table tracks the carrying value, cash interest, interest expense, and discount or premium amortization for each period.

How do you record accrued interest at year-end if payment is made the next day?

Debit interest expense, credit discount on bonds payable, and credit interest payable; then, when paid, debit interest payable and credit cash.

Why is the effective interest method preferred over the straight-line method?

The effective interest method more accurately reflects the true cost of borrowing by matching interest expense to the bond's carrying value and market rate.

Back

Back

04:24

04:24