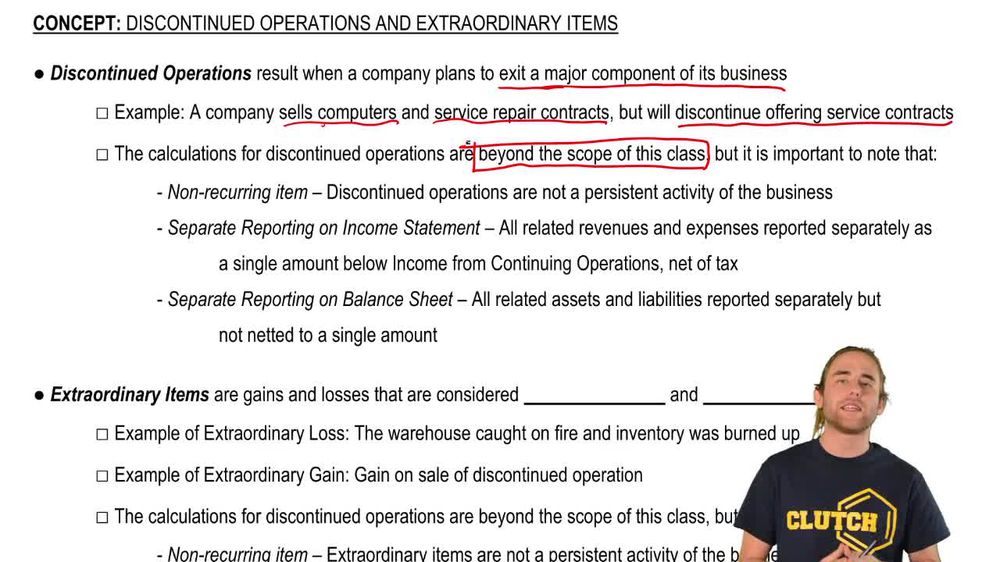

What are discontinued operations in the context of financial accounting?

Discontinued operations refer to parts of a business that a company plans to exit, such as discontinuing a product line or service, but not the entire business.

Where are discontinued operations presented on the income statement?

They are presented separately at the bottom of the income statement, below income from continuing operations.

How are discontinued operations shown on the income statement in terms of tax?

They are shown as a single amount net of tax.

Are discontinued operations considered recurring or non-recurring items?

Discontinued operations are non-recurring items, meaning they are not expected to happen regularly.

Where can you find the details of discontinued operations in financial statements?

Details are typically provided in the footnotes of financial statements, not in the main body of the income statement.

How are assets and liabilities related to discontinued operations shown on the balance sheet?

They are shown separately from regular assets and liabilities, but not netted as a single amount.

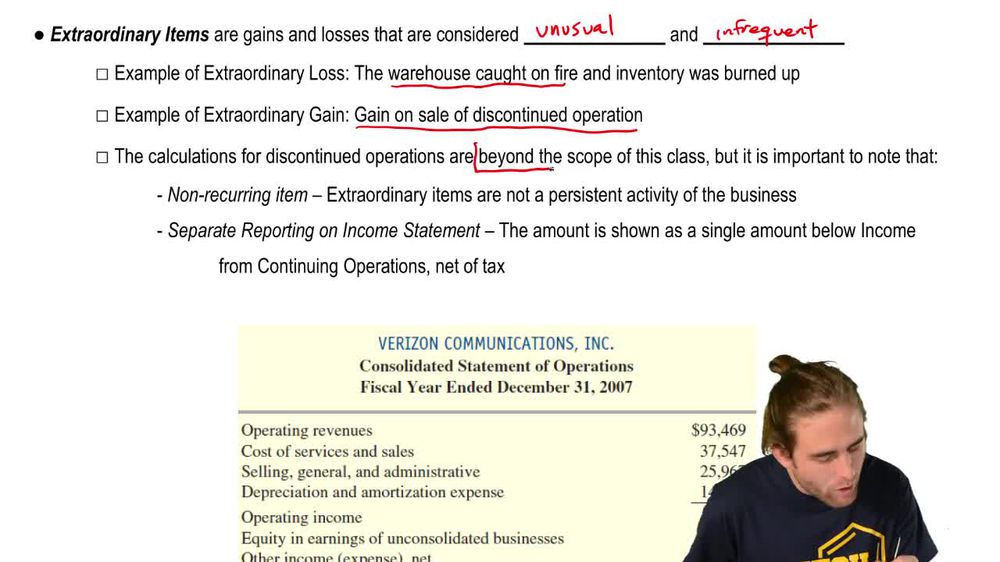

What is an extraordinary item in financial accounting?

An extraordinary item is a gain or loss that is both unusual and infrequent, such as a loss from a warehouse fire or a gain from selling a business segment.

How are extraordinary items presented on the income statement?

They are shown separately at the bottom of the income statement, below continuing operations, as a single amount net of tax.

Are extraordinary items expected to occur regularly in a business?

No, extraordinary items are non-recurring and are not expected to happen every year.

Give an example of an extraordinary loss.

An example is a loss from a warehouse fire that destroys inventory.

Give an example of an extraordinary gain.

An example is a gain from the sale of a discontinued business segment.

Why are discontinued operations and extraordinary items shown separately from continuing operations?

They are shown separately to avoid muddling the income statement and to clearly distinguish non-recurring items from ongoing business activities.

How often do extraordinary items appear on income statements in the real world?

Extraordinary items rarely appear on income statements because such events are very uncommon.

What information is typically shown for discontinued operations and extraordinary items on the income statement?

Only a single net-of-tax amount is shown for each, with further details available in the footnotes.

What is the main purpose of separating discontinued operations and extraordinary items on financial statements?

The main purpose is to provide a clearer picture of the company's ongoing performance by isolating non-recurring events.

Back

Back

03:03

03:03